Commodities & Precious Metals Weekly Report: Apr 22

Posted:

Key points

Energy prices moved lower last week, once again led by natural gas prices. July WTI and Brent crude oil futures prices fell 4 ¼ percent and gasoline prices dropped 2 ¼ percent. Natural gas prices fell 10%.

Energy prices moved lower last week, once again led by natural gas prices. July WTI and Brent crude oil futures prices fell 4 ¼ percent and gasoline prices dropped 2 ¼ percent. Natural gas prices fell 10%.- Grain prices were mixed with wheat prices lower and corn and soybean prices higher. Chicago and Kansas wheat prices fell 3% and 1%, respectively, while corn prices increased 1.5% and soybean prices fell 1%.

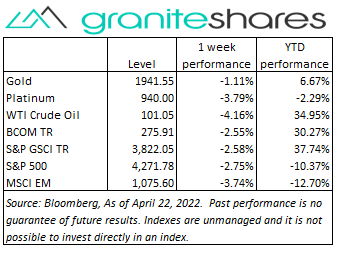

- Precious metal prices moved lower. Spot gold prices lost 2.2% and platinum and silver prices dropped 6%.

- Base metal prices were mostly lower. Aluminum and copper prices fell 1.2% and 2.9%, respectively. Nickel prices were almost unchanged at down 0.2% and zinc prices rose just under 1%.

- The Bloomberg Commodity Index fell 2.6%. 75% of the decrease came from the energy sector with most of the remaining decrease coming from the precious metals sector. The grains and livestock sectors moved slightly higher on the week.

- Strong inflows into gold ($525m), broad commodity ($435m) and silver ($318m) commodity ETPs. Crude oil (-$88m) ETPs experienced the only significant outflows.

Commentary

U.S. stock markets moved lower in another volatile week spurred by hawkish comments from Fed Chairman Powell and outlier weak earnings from Netflix, Verizon and Universal Health Services (Netflix plummeted 35% Wednesday after its after-hours earnings release Tuesday). All three major stock market indexes were higher through Wednesday with risk-on sentiment increasing after two weeks of drawdowns and with sharply falling oil prices. Chairman Powell’s comments on Thursday proclaiming the need to immediately tame inflation and stating a 50bp increase is being considered in May pushed markets sharply lower over Thursday and Friday with the Nasdaq Composite Index, for example, losing over 4.5% over those two days. The Dow Jones Industrial Average continued to outperform both the Nasdaq Composite and S&P 500 Indexes. Rising 10-year U.S. Treasury rates, reaching a high of 2.94% Tuesday, reflecting investor concerns of continued high inflation and rising real yields, increased expectations of slowing economic growth and even of a recession. While the 10-year U.S Treasury rate ended the week off its intraweek high, it closed 8bps higher due entirely to rising 10-year inflation expectations. At week’s end, the S&P 500 Index decreased 2.8% to 4,271.78, the Nasdaq Composite Index fell 3.8% to 12,839.29, the Dow Jones Industrial Average dropped 1.9% to 33,813.44, the 10-year U.S. Treasury rate rose 8 bps to 2.91% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) strengthened 0.9%.

U.S. stock markets moved lower in another volatile week spurred by hawkish comments from Fed Chairman Powell and outlier weak earnings from Netflix, Verizon and Universal Health Services (Netflix plummeted 35% Wednesday after its after-hours earnings release Tuesday). All three major stock market indexes were higher through Wednesday with risk-on sentiment increasing after two weeks of drawdowns and with sharply falling oil prices. Chairman Powell’s comments on Thursday proclaiming the need to immediately tame inflation and stating a 50bp increase is being considered in May pushed markets sharply lower over Thursday and Friday with the Nasdaq Composite Index, for example, losing over 4.5% over those two days. The Dow Jones Industrial Average continued to outperform both the Nasdaq Composite and S&P 500 Indexes. Rising 10-year U.S. Treasury rates, reaching a high of 2.94% Tuesday, reflecting investor concerns of continued high inflation and rising real yields, increased expectations of slowing economic growth and even of a recession. While the 10-year U.S Treasury rate ended the week off its intraweek high, it closed 8bps higher due entirely to rising 10-year inflation expectations. At week’s end, the S&P 500 Index decreased 2.8% to 4,271.78, the Nasdaq Composite Index fell 3.8% to 12,839.29, the Dow Jones Industrial Average dropped 1.9% to 33,813.44, the 10-year U.S. Treasury rate rose 8 bps to 2.91% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) strengthened 0.9%.

Crude oil prices moved lower last week pressured by growing concerns of weak demand. Up 1% Monday on Libyan production outages, crude oil prices fell nearly 5% Tuesday after the IMF and the World Bank significantly lowered its economic growth forecast citing effects from the Russian-Ukraine war and inflation. Supply concerns pushed prices higher Thursday following Wednesday’s much greater-than-expected decline in U.S. oil inventories and renewed EU efforts to ban oil imports from Russia. Demand concerns ruled Friday with Chinese Covid-related lockdowns and Fed Chairman Powell’s hawkish comments Thursday increasing expectations of slower economic growth and, thus, lower demand for oil. On the week, WTI and Brent crude oil prices fell a little over 4%. A volatile week for natural gas prices, rising over 7% Monday then falling almost 9% Tuesday, losing 3% Wednesday and dropping 6% Friday. Concerns of strong demand, tight supply and cold weather Monday were replaced by forecasts of warmer weather, a larger-than-expected increase in inventories and Fed rate hike concerns pushing natural gas prices 10% lower on the week.

Pressured by hawkish comments from Fed governors on Tuesday and Wednesday and then again on Thursday by Fed Chairman Powell, spot gold prices ended the week over 2% lower. 10-year real yields rose 9bps to 0% Tuesday following FOMC member Bullard’s call for a Fed funds rate of 3.5% by year end and pushed gold prices nearly 1.5% lower. Chairman Powell’s comments Thursday saying inflation needed to be addressed now and that a 50bp rate hike was a possibility in May helped pressure prices even lower. The decline in gold prices occurred despite the fact the 10-year real yields ended the week unchanged (at -0.08%) and 10-year inflation expectations increased 8bps to 2.99%. Silver and Platinum prices fell with gold prices.

Base metal prices, higher through Thursday mainly on supply concerns, fell markedly Friday, pushing most prices lower on the week. Supply concerns stemming from Russia-Ukraine repercussions and already historically low inventory levels were overruled Friday by Chinese Covid-related demand destruction, a stronger U.S. dollar and growing concerns of reduced global growth due to central bank tightening policies. Zinc prices, however, ended the week higher, supported by extremely tight supply conditions.

Grain prices benefited from U.S. adverse weather conditions, poor crop conditions and slow planting progess. Reports Russia may be exporting more wheat than estimated as well as weak wheat exports, pushed wheat prices lower on the week. Corn and soybean prices finished higher on the week supported by stronger export demand.

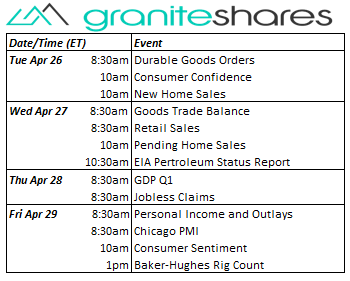

Coming up this week

Busier data-week with new and pending home sales, consumer confidence and sentiment, retail sales and the first estimate of Q1 GDP (Thursday).

Busier data-week with new and pending home sales, consumer confidence and sentiment, retail sales and the first estimate of Q1 GDP (Thursday).- Durable Goods Orders, Consumer Confidence and New Home Sales on Tuesday.

- Goods Trade Balance, Retail Sales, Pending Home Sales on Wednesday.

- Q1 GDP and Jobless Claims on Thursday.

- Personal Income and Outlays, Chicago PMI and Consumer Sentiment on Friday.

- EIA Petroleum Status Report Wednesday and Baker-Hughes Rig Count on Friday.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.