Commodities & Precious Metals Weekly Report: Apr 29

Posted:

Key points

Energy prices were higher last week. Natural gas prices rose the most, gaining just shy of 9%, followed by heating oil prices, up almost 7%. Gasoline prices rose 4% and WTI and Brent crude oil prices gained 2% and 1%, respectively.

Energy prices were higher last week. Natural gas prices rose the most, gaining just shy of 9%, followed by heating oil prices, up almost 7%. Gasoline prices rose 4% and WTI and Brent crude oil prices gained 2% and 1%, respectively. - Lean hog prices dropped over 10% and live cattle prices lost 4%.

- Grain prices were mixed with wheat prices, once again, lower and corn prices higher. Chicago and Kansas wheat prices fell 2% and 4%, respectively, while corn prices increased 3%. Soybean prices fell less than ¼ percent.

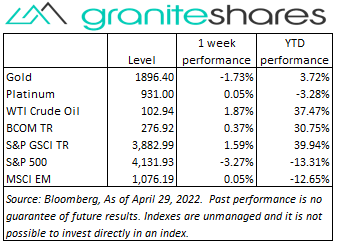

- Precious metal prices were mixed. Spot gold prices lost 1.7%, spot silver prices fell 5.6%. Spot platinum prices were unchanged.

- Base metal prices were all lower. Aluminum and zinc prices fell 6.1% and 7.4%, respectively. Nickel and copper prices were down a little over 4%.

- The Bloomberg Commodity Index increased 0.4%. Energy sector gains were partially offset by losses in the livestock, base metal and precious metal sectors.

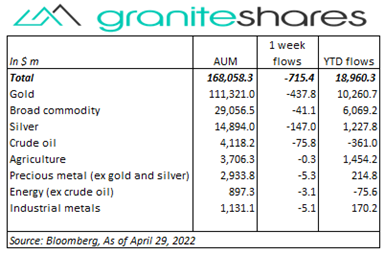

- A week of outflows from commodity ETPs Gold ETPs saw outflows of $438 million, silver ETPs $147 million and crude oil ETPs $76 million.

Commentary

A very volatile week for U.S. stock markets with the S&P 500 Index recording 2.5% or greater moves 3 days last week and the Nasdaq Composite Index registering two 4% moves and one 3% move. All three major stock indexes fell significantly last week with the Nasdaq Composite Index underperforming the both the S&P 500 Index and the Dow Jones Industrial Average. Stock markets were battered by a combination of investor concerns including continued elevated inflation levels, this Tuesday’s FOMC meeting and expectations of an aggressively tightening Fed, slowing Chinese economic growth and weaker-than-expected earnings reports. These concerns, more or less, translate into fears of weaker U.S. economic growth or recession pressuring stock valuations (especially for tech stocks) lower. Thursday’s surprise Q1 GDP contraction along with Friday’s elevated PCE Price Index release seemed to support these concerns as did earnings misses from Alphabet, Microsoft and Amazon. 10-year U.S. Treasury rates rose slightly last week but the increase came as real rates rose and inflation expectations fell, perhaps reflecting expectations inflation levels may have peaked. 10-year real rates closed the week at 0% while 10-year inflation expectations finished at 2.94%. The U.S. dollar sharply increased last week mirroring the rise in 10-year real rates. At week’s end, the S&P 500 Index decreased 3.2% to 4,131.93, the Nasdaq Composite Index fell 3.9% to 12,334.64, the Dow Jones Industrial Average dropped 2.5% to 32,978.52, the 10-year U.S. Treasury rate rose 3 bps to 2.94% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) strengthened 2.0%.

A very volatile week for U.S. stock markets with the S&P 500 Index recording 2.5% or greater moves 3 days last week and the Nasdaq Composite Index registering two 4% moves and one 3% move. All three major stock indexes fell significantly last week with the Nasdaq Composite Index underperforming the both the S&P 500 Index and the Dow Jones Industrial Average. Stock markets were battered by a combination of investor concerns including continued elevated inflation levels, this Tuesday’s FOMC meeting and expectations of an aggressively tightening Fed, slowing Chinese economic growth and weaker-than-expected earnings reports. These concerns, more or less, translate into fears of weaker U.S. economic growth or recession pressuring stock valuations (especially for tech stocks) lower. Thursday’s surprise Q1 GDP contraction along with Friday’s elevated PCE Price Index release seemed to support these concerns as did earnings misses from Alphabet, Microsoft and Amazon. 10-year U.S. Treasury rates rose slightly last week but the increase came as real rates rose and inflation expectations fell, perhaps reflecting expectations inflation levels may have peaked. 10-year real rates closed the week at 0% while 10-year inflation expectations finished at 2.94%. The U.S. dollar sharply increased last week mirroring the rise in 10-year real rates. At week’s end, the S&P 500 Index decreased 3.2% to 4,131.93, the Nasdaq Composite Index fell 3.9% to 12,334.64, the Dow Jones Industrial Average dropped 2.5% to 32,978.52, the 10-year U.S. Treasury rate rose 3 bps to 2.94% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) strengthened 2.0%.

Sharply lower Monday on increased concerns of slower economic growth both due to Covid-related lockdowns in China and central bank tightening (especially by the Fed), crude oil prices moved higher the remainder of the week buoyed by renewed supply concerns. Germany’s willingness to embargo Russian oil purchases, a smaller-than-expected increase in U.S. oil inventories and OPEC+’s continued refusal to increase production all lent support to oil prices. In addition, Russia’s halting of natural gas sales to Poland and Bulgaria not only helped move natural gas prices higher but also pushed diesel and heating oil prices higher (they are used as substitutes for natural gas), in turn supporting oil prices. China’s Politburo’s plans to support the Chinese economy during its Covid-related lockdowns also supported prices. WTI crude oil prices finished the week 2% higher. Natural gas prices continued their climb higher benefiting from colder-than-normal weather and expectations of increased LNG exports.

Gold prices moved lower last week pressured by a sharply strengthening U.S. dollar. Growing concerns of aggressive Fed tightening (the FOMC meets beginning this Tuesday with a rate decision Wednesday), pushing 10-year real yields toward 0% and buoying the U.S. dollar, worked to move gold prices lower. Nonetheless, continued Russia-Ukraine war concerns, continued elevated inflation levels, an unexpected contraction in Q1 GDP and China’s Covid-related lockdowns helped floor losses. Silver prices fell with gold and base metal prices.

Base metal prices moved lower last week pressured by growing demand concerns due to China’s Covid-related lockdowns and, to a lesser extent, by central bank tightening. Prices experienced a slight reprieve Wednesday, moving higher following China’s Politburo’s announcement it would support the economy, but resumed their move lower the remainder off the week. A strong U.S. dollar also contributed to weaker prices.

Wheat prices moved lower last week pressured by better-than-expected planting progress in Ukraine and larger-than-expected planting acreage in Canada. Corn prices, higher on the week, benefited from poor planting progress and adverse actual and forecasted weather conditions. Soybean prices, slightly lower on the week, were supported by continued South America weather concerns and decent export numbers.

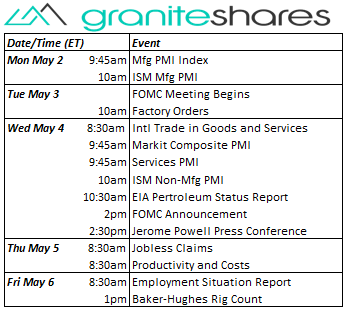

Coming up this week

Busy data-week filled with service and manufacturing PMI releases and highlighted by an FOMC rate decision Wednesday and Friday’s Unemployment Report.

Busy data-week filled with service and manufacturing PMI releases and highlighted by an FOMC rate decision Wednesday and Friday’s Unemployment Report. - Mfg PMI and ISM Mfg Indexes on Monday.

- FOMC Meeting Begins and Factory Orders on Tuesday.

- Intl Trade in Goods and Services, PMI releases, FOMC Announcement and Jerome Powell Press Conference on Wednesday.

- Jobless Claims and Productivity and Costs on Thursday.

- Employment Situation Report on Friday.

- EIA Petroleum Status Report Wednesday and Baker-Hughes Rig Count on Friday.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.