Commodities & Precious Metals Weekly Report: Aug 5

Posted:

Key points

Energy prices all fell last week. WTI and Brent crude oil, gasoline and heating oil prices fell between 8% and 10%. Natural gas prices were lower by 2%.

Energy prices all fell last week. WTI and Brent crude oil, gasoline and heating oil prices fell between 8% and 10%. Natural gas prices were lower by 2%.- Grain prices were lower as well. Wheat prices fell between 3% and 4%, soybean prices were down 4% and corn prices lost 1%.

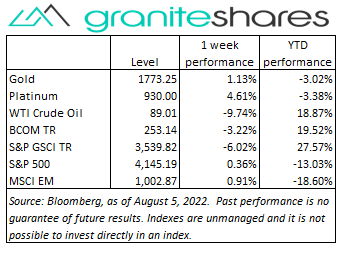

- Precious metal prices were mixed. Spot gold prices increased 0.6% and spot platinum prices rose 4.4%. Spot silver prices were down 2%.

- Base metal prices were mainly lower. Nickel prices fell 6%, aluminum prices lost 3% and copper prices gave up 1%. Zinc prices rose 6%.

- The Bloomberg Commodity Index fell 3.2%. The energy sector was primarily responsible for the decline.

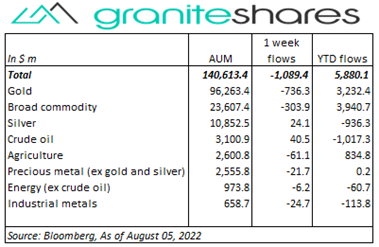

- $1.1 billion outflows from commodity ETPs last week, predominantly from gold and broad commodity ETPs.

Commentary

Stock prices mainly moved higher last week with the Nasdaq Composite Index strongly outperforming the Dow Jones Industrial Average and the SP 500 Index. The Dow Jones Industrial Average finished slightly lower on the week. Geo-political concerns dominated stock markets early in the week. Speaker of the House Nancy Pelosi’s visit to Taiwan and China’s strong condemnation of it pushed stock prices lower and bond and gold prices higher as investors sought haven-type investments. Wednesday’s strong ISM Services report and Friday’s much better-than-expected jobs report renewed concerns of continued aggressive Fed tightening capping stock gains, driving the 10-year Treasury rate higher and strengthening the U.S. dollar. The 10-year Treasury rate increased 17bps over the week with a 25bp increase in 10-year real rates offset by an 8bp decline in 10-year inflation expectations. For the week, the S&P 500 Index increased 0.4% to 4,145.19, the Nasdaq Composite Index rose 2.1% to 12,657.55, the Dow Jones Industrial Average edged lower 0.1% to 32,801.51, the 10-year U.S. Treasury rate rose 17bps to 2.82% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) strengthened 0.7%.

Stock prices mainly moved higher last week with the Nasdaq Composite Index strongly outperforming the Dow Jones Industrial Average and the SP 500 Index. The Dow Jones Industrial Average finished slightly lower on the week. Geo-political concerns dominated stock markets early in the week. Speaker of the House Nancy Pelosi’s visit to Taiwan and China’s strong condemnation of it pushed stock prices lower and bond and gold prices higher as investors sought haven-type investments. Wednesday’s strong ISM Services report and Friday’s much better-than-expected jobs report renewed concerns of continued aggressive Fed tightening capping stock gains, driving the 10-year Treasury rate higher and strengthening the U.S. dollar. The 10-year Treasury rate increased 17bps over the week with a 25bp increase in 10-year real rates offset by an 8bp decline in 10-year inflation expectations. For the week, the S&P 500 Index increased 0.4% to 4,145.19, the Nasdaq Composite Index rose 2.1% to 12,657.55, the Dow Jones Industrial Average edged lower 0.1% to 32,801.51, the 10-year U.S. Treasury rate rose 17bps to 2.82% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) strengthened 0.7%.

Sharply lower oil prices last week driven both by demand and supply concerns. Weak manufacturing data in Europe, the U.S. and Asia added to already existing recession concerns while Wednesday’s surprise large increase in crude oil and gasoline inventories contributed to supply-side anxiousness. The BoE’s recession warning following its 50bp rate increase also pressured prices lower. Friday’s much stronger-than-expected jobs reports moved oil prices slightly higher.

Gold prices moved higher again last week buoyed mainly by increased tensions between the U.S. and China resulting from Speaker of the House Pelosi’s visit to Taiwan. Prices gains were capped, however, by renewed concerns of continued aggressive Fed tightening following Friday’s much stronger-than-expected jobs report as well as comments earlier in the week from Fed presidents insisting the Fed would continue to remain vigilant. Consequently, 10-year real yields, increased 25bps, closing the week at 0.35% and the U.S. dollar strengthened 0.7%.

Base metal prices were mainly lower last week, influenced by global recession concerns and risk-off sentiment due to increased U.S. – China tensions. Weaker-than-expected manufacturing activity in Europe, the U.S. and Asia initially added to global growth slowdown concerns while Friday’s much stronger-than-expected jobs report increased expectations of stronger base metal demand. Increased expectations of continued Fed aggressive rate policy strengthened the U.S. dollar pressuring base metal prices lower as well.

Grain prices fell last week. Improved U.S. weather forecasts, better-than-expected crop ratings and wheat shipments from the Ukraine all acted to push prices lower. A stronger U.S. dollar and increased tensions between the U.S. and China also contributed to lower prices.

Coming up this week

Very light data week but charged with CPI and PPI releases Wednesday and Thursday.

Very light data week but charged with CPI and PPI releases Wednesday and Thursday.- Productivity on Tuesday.

- CPI on Wednesday.

- PPI and Jobless Claims on Thursday.

- Export and Import Prices and Consumer Sentiment on Friday.

- EIA Petroleum Status Report Wednesday and Baker-Hughes Rig Count on Friday.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.