Commodities & Precious Metals Weekly Report: Jun 3

Posted:

Key points

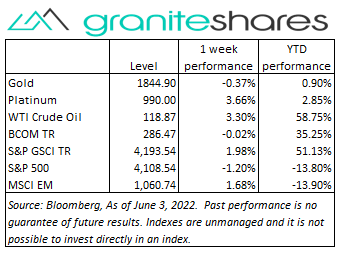

Energy prices were sharply higher again. Gasoil, heating oil and gasoline prices increased the most – again - gaining 12%, 10% and 9%, respectively. WTI and Brent crude oil prices increased 3.3% and 3.8%, respectively.

Energy prices were sharply higher again. Gasoil, heating oil and gasoline prices increased the most – again - gaining 12%, 10% and 9%, respectively. WTI and Brent crude oil prices increased 3.3% and 3.8%, respectively. - Grain prices were sharply lower. Wheat prices fell between 9% and 10%, corn prices dropped almost 7% and soybean prices lost 2%.

- Precious metal prices were mixed. Spot gold prices were slightly lower at down 0.1% and spot silver prices fell 1.3%. Spot platinum prices jumped 7.0% higher.

- Base metal prices were mixed as well though aluminum, zinc and nickel prices didn’t trade Thursday and Friday. Copper prices increased almost 4% and zinc prices increased less than 1%. Aluminum prices fell 5% and nickel prices lost 0.6%.

- The Bloomberg Commodity Index was basically unchanged. Gains in the energy sector were almost entirely offset by losses in the grains sector.

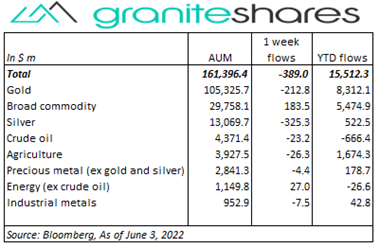

- Small outflows (-$389m) from commodity ETPs last week. Gold (-$212m) and silver (-$389m) ETP outflows were partially offset by broad commodity ($184m) inflows.

Commentary

A choppy week for U.S. stock markets with investor sentiment pushed and pulled by uncertainty surrounding the Fed’s tightening of monetary policy, the trajectory of inflation, the strength of the economy and whether major stock market indexes have bottomed. Down almost 1.5% through Wednesday, the S&P 500 Index rose just under 2% Thursday, buoyed by hopes of a slowing economy and peaking inflation following a much weaker-than-expected ADP jobs number released Wednesday. That sentiment was reversed Friday after the release of the Non-Farm Payroll report showing larger-than-expected job growth and continued wage pressures. The 10-yearr U.S Treasury rate rose 20bps last week, with slightly more than half of the increase coming from rising inflation expectation and slightly less than half coming from rising real rates. At week’s end, the S&P 500 Index fell 1.2% to 4,108.54, the Nasdaq Composite Index lost 1.0% to close at 12,012.73, the Dow Jones Industrial Average decreased 1.0% to 32,989.91, the 10-year U.S. Treasury rate jumped 20 bps to 2.94% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) strengthened 0.4%.

A choppy week for U.S. stock markets with investor sentiment pushed and pulled by uncertainty surrounding the Fed’s tightening of monetary policy, the trajectory of inflation, the strength of the economy and whether major stock market indexes have bottomed. Down almost 1.5% through Wednesday, the S&P 500 Index rose just under 2% Thursday, buoyed by hopes of a slowing economy and peaking inflation following a much weaker-than-expected ADP jobs number released Wednesday. That sentiment was reversed Friday after the release of the Non-Farm Payroll report showing larger-than-expected job growth and continued wage pressures. The 10-yearr U.S Treasury rate rose 20bps last week, with slightly more than half of the increase coming from rising inflation expectation and slightly less than half coming from rising real rates. At week’s end, the S&P 500 Index fell 1.2% to 4,108.54, the Nasdaq Composite Index lost 1.0% to close at 12,012.73, the Dow Jones Industrial Average decreased 1.0% to 32,989.91, the 10-year U.S. Treasury rate jumped 20 bps to 2.94% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) strengthened 0.4%.

Supported by the end of Shanghai Covid-related lockdowns, the EU formally agreeing to ban 90% of Russian oil by year’s end, much lower-than-expected inventory levels and economic reports indicating a strong economy, WTI crude oil prices increased north of 3% last week. The increase came despite OPECs 50% increase of planned monthly production increases and despite a significant increase in U.S. oil production. Gasoline and heating oil prices increased much more than WTI crude oil prices, driven higher by strong demand, historically low inventory levels and constrained refining capacity. Gasoline and heating oil prices rose close to 9%.

A somewhat volatile week for gold prices, seesawing with rising and falling longer-term interest rates and a vacillating U.S. dollar. Gold prices fell 1% Tuesday, pressured by a 10bp increase in the 10-year U.S. Treasury rate, only to increase almost 2% over Wednesday and Thursday following a much weaker-than-expected ADP jobs number precipitating increased expectations of a slowing economy. Friday’s much better-than-expected Non-Farm Payroll Report squelched those expectations and gave rise – again – to concerns of a strong economy permitting the Fed to tighten aggressively. Platinum prices jumped 7% higher, powered by expectations of strong auto-related demand. While 10-year U.S. Treasury rates increased 20bps over the week, slightly more than half of that increase came from rising inflation expectations. The 10-year real yield, while substantively off its low, is still at a highly accommodative level of 18bps.

Copper prices moved higher again last week, boosted by China’s apparent end of lockdowns and by Chinese stimulus measures. Sharply lower production levels from Chilean mines also boosted prices, with copper prices rising more than 5% on Wednesday. Aluminum prices fell again last week, continuing to suffer from high energy-related production costs and weak demand. The LME was closed Thursday and Friday due to the Queen’s Platinum Jubilee celebrations.

Grain prices were all lower last week, led by a sharp decline in wheat prices. Chicago HRW wheat prices fell over 11% through Tuesday, suffering from Russia’s claims it will allow Ukrainian wheat to be shipped and as a result of good planting progress and forecasted weather in the U.S. Corn prices moved lower (down 6.5% on the week) on good planting progress and favorable weather forecasts as well. News of a fund liquidating corn and wheat positions Tuesday and Wednesday also may have pressured prices lower. Soybean prices, down about 2%, benefited from strong exports demand.

Coming up this week

Very light data week with CPI, released Friday, headlining.

Very light data week with CPI, released Friday, headlining.- Intl Trade in Goods and Services on Tuesday.

- Jobless Claims on Thursday.

- CPI and Consumer Sentiment on Friday..

- EIA Petroleum Status Report Wednesday and Baker-Hughes Rig Count on Friday.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.