Commodities & Precious Metals Weekly Report: Mar 18

Posted:

Key points

Energy prices were mixed last week. May WTI and Brent crude oil futures prices decreased close to 3% and gasoline prices fell 2.3%. Heating oil and gasoil prices rose 2.7% and 1.9%, respectively. Natural gas prices increased 2.9%.

Energy prices were mixed last week. May WTI and Brent crude oil futures prices decreased close to 3% and gasoline prices fell 2.3%. Heating oil and gasoil prices rose 2.7% and 1.9%, respectively. Natural gas prices increased 2.9%.- Grain prices were all lower. Chicago and Kansas wheat prices fell 3.9% and 1.7%, respectively. Corn and soybean prices lost 2.7% and 0.5%, respectively.

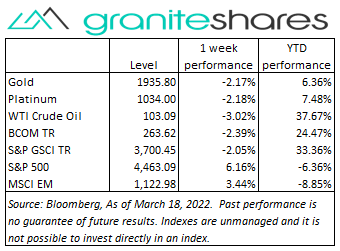

- Precious metal prices were all lower, too. June gold futures prices fell 2.8% and May silver futures prices lost 4.1%. Platinum prices fell 2.2% and palladium prices lost over 11%.

- Base metal prices were mixed. Nickel prices dropped 23% (following the resumption of trading Wednesday) and aluminum prices lost 3%. Copper and zinc prices increased 2.5% and 0.5%, respectively.

- The Bloomberg Commodity Index decreased 2.4%. The drop in nickel prices was responsible for almost half of the decline with the grains and energy sectors also detracting from performance.

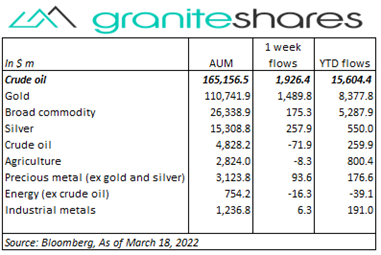

- Decent flows into commodity ETPs last week with gold ($1,490m) ETP inflows leading the way. Silver and broad commodity ETPs saw inflows of $258 million and $175 million, respectively. Crude oil ETPs experienced $72 million of outflows.

Commentary

Volatility continued last week but this time with all three major U.S. stock indexes finishing significantly higher. Uncertainty surrounding the FOMC announcement Wednesday and continued concerns regarding the war in Ukraine pushed markets lower Monday, the only down day of the week. Sharply falling oil prices (through Wednesday) and the FOMC decision to raise the Fed Funds target rate range to 0.25% - 0.50% boosted risk-on sentiment driving stock markets 1% - 2% higher each day the remainder of the week. The FOMC announcement Wednesday was deemed to hold no real surprises with the Fed holding off from increasing the Fed Funds target range by 50bps but indicating it may raise rates by 25bps in each of the remaining meetings this year while at some point beginning the process of reducing its balance sheet. Reports of progress in negotiations between the Ukraine and Russia earlier in the week faded as the week progressed and oil prices, down 12% through Wednesday, rallied sharply Thursday and Friday. Nonetheless, U.S. stock markets continued to rise, focusing more, instead, on the FOMC decision and announcement. The 10-year U.S. Treasury rate rose 16bps powered by a 23bp increase in real yields and a slight decline in 10-year inflation breakeven rates to 2.9%. The increase in real rates was more a result of falling haven-investment demand, however, than of the FOMC decision. For the week, the S&P 500 rose 6.2% to 4,463.09, the Nasdaq Composite Index jumped 8.2% to 13,892.84, the Dow Jones Industrial Average gained 5.5% to close at 34,749.36, the 10-year U.S. Treasury rate increased 16bp to 2.16% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) weakened 0.9%.

Volatility continued last week but this time with all three major U.S. stock indexes finishing significantly higher. Uncertainty surrounding the FOMC announcement Wednesday and continued concerns regarding the war in Ukraine pushed markets lower Monday, the only down day of the week. Sharply falling oil prices (through Wednesday) and the FOMC decision to raise the Fed Funds target rate range to 0.25% - 0.50% boosted risk-on sentiment driving stock markets 1% - 2% higher each day the remainder of the week. The FOMC announcement Wednesday was deemed to hold no real surprises with the Fed holding off from increasing the Fed Funds target range by 50bps but indicating it may raise rates by 25bps in each of the remaining meetings this year while at some point beginning the process of reducing its balance sheet. Reports of progress in negotiations between the Ukraine and Russia earlier in the week faded as the week progressed and oil prices, down 12% through Wednesday, rallied sharply Thursday and Friday. Nonetheless, U.S. stock markets continued to rise, focusing more, instead, on the FOMC decision and announcement. The 10-year U.S. Treasury rate rose 16bps powered by a 23bp increase in real yields and a slight decline in 10-year inflation breakeven rates to 2.9%. The increase in real rates was more a result of falling haven-investment demand, however, than of the FOMC decision. For the week, the S&P 500 rose 6.2% to 4,463.09, the Nasdaq Composite Index jumped 8.2% to 13,892.84, the Dow Jones Industrial Average gained 5.5% to close at 34,749.36, the 10-year U.S. Treasury rate increased 16bp to 2.16% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) weakened 0.9%.

A volatile week for oil prices as well. WTI oil prices fell 12% through Wednesday pushed lower by reports of good progress in Russia-Ukraine negotiations and news of additional Chinese Covid-19 lockdowns. A larger-than-expected gain in U.S. oil inventories reported Wednesday by the EIA also contributed to lower prices. Thursday saw WTI prices jump over 8.5% higher following an IEA report stating oil supplies could be depressed by a greater-than-expected 3 million barrels/day by de-facto sanctioning of Russian oil. WTI oil prices moved another 1.5% higher Friday on lessened hopes of a Russia-Ukraine negotiated agreement to end the conflict and on reports of new Chinese economic stimulus programs. For the week, WTI and Brent crude oil prices fell 3.0% and 3.4%, respectively.

Down 3.5% through Tuesday, gold prices increased just under 1.5% Wednesday and Thursday following Wednesday’s FOMC announcement and rate increase and as oil prices jumped markedly higher, a combination that seemed to elevate concerns of stagflation. Spot gold prices ended the week down 3.2%. Platinum and silver prices followed gold prices. Palladium prices fell nearly 12% over the week, dropping 15% on Monday as concerns regarding Russian supplies eased.

LME nickel trading resumed Wednesday with nickel prices falling limit down Wednesday, Thursday and Friday to finish the week 23% lower. The limit-down trading occurred as LME prices sought equilibrium with Shanghai-traded nickel prices. Copper prices fell early in the week following reports of planned Chinese Covid-19-related lockdowns and on increased hopes of a ceasefire agreement between Russia and Ukraine. Copper prices rose the remainder of the week (to finish the week higher) following suspension of copper production at a Southern Copper mine in Peru. Aluminum prices ended lower on the week, faltering with concerns of slower Chinese economic growth and on increased hopes of a Russia-Ukraine ceasefire.

Another very volatile week for grains. Chicago wheat prices, 3% lower on the week, moved over 5% higher Tuesday on estimates Ukraine new crop wheat production could be 40% lower than last year then fell 7% Wednesday on reports a Russia -Ukraine ceasefire agreement was close. Thursday saw wheat prices increase about 2.5% on renewed supply concerns. Corn prices moved similarly but with less volatility. Soybean prices, down about ½ percent on the week, were supported by good export demand and late-week rising oil prices.

Coming up this week

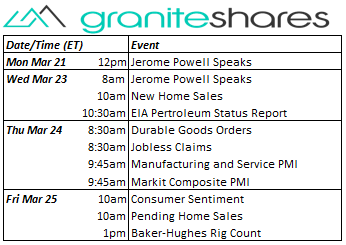

Decent data-week with Fed Chair Powell speaking Monday and Wednesday, housing data Wednesday and Friday and Durable Goods Orders Thursday.

Decent data-week with Fed Chair Powell speaking Monday and Wednesday, housing data Wednesday and Friday and Durable Goods Orders Thursday.- Jerome Powell Speaks on Monday

- Jerome Powell Speak and New Home Sales on Wednesday.

- Durable Goods Orders, Jobless Claims, Mfg and Services PMI and Markit Composite Flash on Thursday.

- Consumer Sentiment and Pending Home Sales on Friday.

- EIA Petroleum Status Report Wednesday and Baker-Hughes Rig Count on Friday.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.