Commodities & Precious Metals Weekly Report: Jan 22

Posted:

Key points

Energy prices were mixed last week. WTI and Brent crude oil prices were down only slightly and gasoline prices increased 1%. Heating oil prices fell ½ percent and natural gas prices dropped almost 9%.

Energy prices were mixed last week. WTI and Brent crude oil prices were down only slightly and gasoline prices increased 1%. Heating oil prices fell ½ percent and natural gas prices dropped almost 9%. - Grain prices erased the previous week’s gains, declining significantly last week. Soybean prices decreased the most, falling nearly 7.5%. Chicago wheat prices fell 6% and Kansas wheat prices dropped 4.5%. Corn prices decreased almost 6%.

- Base metal prices were all higher with nickel prices increasing the most. Nickel prices increased 1.5% and copper and zinc prices gained about 0.6% Aluminum prices were only slightly higher, increasing 0.1%.

- Precious metal prices were all higher last week with silver prices leading the way. Silver prices increased just under 3% and gold and platinum prices rose about ¾ percent.

- Dragged down by negative grains and energy sector performance, the Bloomberg Commodity Index decreased 1.7% last week. Positive precious metal, softs and livestock sector returns partially offset losses in the energy and grains sectors.

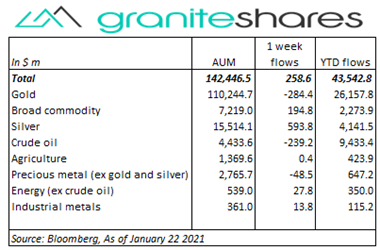

- Relatively benign increase in Commodity ETP assets with inflows of about $260 million. However, flows were splintered. Silver ETP inflows amounted to almost $600 million and broad commodity ETPs had inflows of close to $200 million. Those inflows were partially offset by almost $300 million outflows from gold ETPs and almost $250 million outflows from crude oil ETPs.

Commentary

U.S. stock markets were higher last week with stock prices supported by strong economic reports and hopes of additional stimulus spending. Slightly lower-than-expected jobless claims, a stronger-than-expected PMI Composite Flash Index release and much better-than-expected housing starts and permits and existing home sales combined with Janet Yellen’s call for additional, larger stimulus spending and President Biden’s announcement of a $1.9 trillion stimulus package helped move stock prices higher through most of the week. The Nasdaq Composite Index closed the week at a record high elevated by strong performance by Apple, Amazon, Facebook and Netflix while the S&P 500 Index, hurt by poor IBM and Intel earnings reports, closed just off its record high set Thursday. At week’s end the S&P 500 Index increased 2.0% to 3,841.47, the Nasdaq Composite Index rose 4.2% to 13,543.06, the 10-year U.S. Treasury was unchanged at 1.09% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) weakened 0.6%.

U.S. stock markets were higher last week with stock prices supported by strong economic reports and hopes of additional stimulus spending. Slightly lower-than-expected jobless claims, a stronger-than-expected PMI Composite Flash Index release and much better-than-expected housing starts and permits and existing home sales combined with Janet Yellen’s call for additional, larger stimulus spending and President Biden’s announcement of a $1.9 trillion stimulus package helped move stock prices higher through most of the week. The Nasdaq Composite Index closed the week at a record high elevated by strong performance by Apple, Amazon, Facebook and Netflix while the S&P 500 Index, hurt by poor IBM and Intel earnings reports, closed just off its record high set Thursday. At week’s end the S&P 500 Index increased 2.0% to 3,841.47, the Nasdaq Composite Index rose 4.2% to 13,543.06, the 10-year U.S. Treasury was unchanged at 1.09% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) weakened 0.6%.

Buoyed by hopes of additional, larger U.S. stimulus spending and a weaker U.S. dollar, WTI crude oil prices increased just under 2% through Wednesday. Larger-than-expected inventory levels as reported by both the API late Thursday and the EIA on Friday as wells as demand concerns resulting from additional lockdowns in China pressured WTI prices lower with prices finishing the week basically unchanged.

Gold prices mirrored U.S. stock markets, rising through Thursday on increased expectations of larger, additional stimulus spending and as a result of a weaker U.S. dollar and then moving slightly lower on Friday after a much stronger-than-expected PMI Composite Flash release and some pushback on President Biden’s proposed stimulus package. Platinum and silver prices followed gold prices and moved higher with base metal prices.

Base metal prices moved higher throughout the week, benefiting from growing expectations of additional U.S. stimulus spending, a weaker U.S. dollar and stronger-than-expected U.S. manufacturing activity. Copper and nickel prices were supported also by supply concerns as a result of falling LME copper inventory levels and increasing concerns of nickel mining disruptions in New Caledonia. Copper and nickel prices fell Friday, moving off their week’s highs set Thursday, reacting to increased Chinese lockdowns and weaker-than-expected EU manufacturing numbers.

Grain prices moved significantly lower last week, reversing most of the gains recorded the previous week. Favorable rainfall in South America was primarily the trigger for the steep selloff in corn and soybean prices, with increased corn and soybean plantings in South America adding to supply expectations and helping to offset low global stock levels and forecasted harvest yields. Coronavirus-related demand concerns and reports of new cases of swine flu in China also contributed to lower prices. Wheat prices moved lower with corn and soybean prices on no real news.

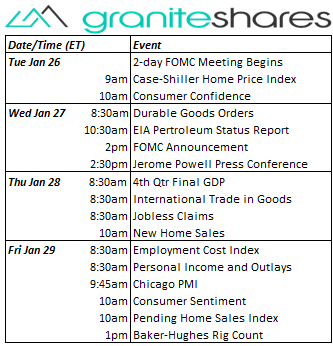

Coming up this week

Busy data-week highlighted by the 2-day FOMC meeting beginning Tuesday.

Busy data-week highlighted by the 2-day FOMC meeting beginning Tuesday. - FOMC meeting begins, Case-Shiller Home Price Index and Consumer Confidence on Tuesday.

- Durable Goods Orders, FOMC Announcement and Jerome Powell Press Conference on Wednesday.

- 4th Qtr Final GDP, International Trade in Goods, Jobless Claims and New Home Sales on Thursday.

- Employment Cost Index, Personal Income and Outlays, Chicago PMI, Consumer Sentiment and Pending New Homes Sales Index on Friday.

- EIA petroleum status report on Wednesday and Baker-Hughes rig count also on Friday.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.