Commoditized Wisdom: Report (Week Ending March 8, 2024)

Posted:

Key points

Energy prices all fell between 2% and 3%.

Energy prices all fell between 2% and 3%.- Grain prices were mostly higher with Kansas City wheat and corn prices gaining 4% and soybean prices rising 3%. Chicago wheat prices fell 4%.

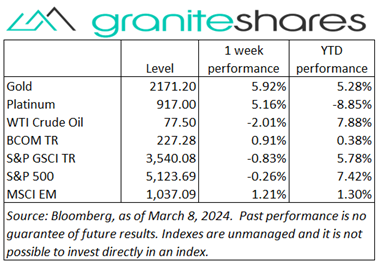

- Spot gold and silver prices rose 5%. Spot platinum prices increased 3% and spot palladium prices gained 7%.

- Except for aluminum, base metal prices were all higher. Zinc and lead prices increased 5% and 3%, respectively. Copper and nickel prices rose 1% and 2%, respectively. Aluminum prices fell 1%.

- The Bloomberg Commodity Index increased 0.9%. Gains in the base and precious metals and grains sectors were only partially offset by losses in the energy sector.

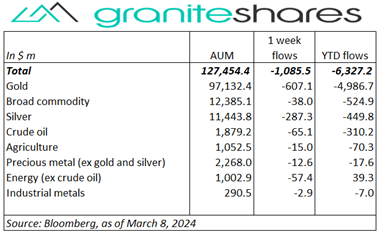

- Outflows from each ETP category but primarily from gold and silver ETPs

Commentary

All 3 major stock indexes finished the week lower, pulling back from recent highs on no real news. Uncertainty before Fed Chair Powell’s testimony before Congress Wednesday and Thursday and Friday’s payroll report reduced risk-on appetite, pushing all 3 indexes at least 1% lower with tech stocks (excluding Nvidia) bearing the brunt of the downturn and as a result, the Nasdaq Composite Index as well. Powell’s testimony Wednesday and Thursday in which he stated the Fed may soon be in a position to cut rates helped push longer-term Treasury rates lower and stock indexes higher. Friday’s mixed payroll report, showing a larger-than-expected increase in jobs created but slower-than-expected wage growth and a higher-than-expected unemployment rate, ended up moving indexes lower to close the week lower. For the week, the S&P 500 Index decreased 0.3% to 5,123.69, the Nasdaq Composite Index fell 1.2% to 16,085.11, the Dow Jones Industrial Average lost 0.9% to close at 38,723.15, the 10-year U.S. Treasury rate fell 10bp to 4.08% and the U.S. dollar (as measured by the ICE U.S. Dollar index – DXY) weakened 1.1%.

All 3 major stock indexes finished the week lower, pulling back from recent highs on no real news. Uncertainty before Fed Chair Powell’s testimony before Congress Wednesday and Thursday and Friday’s payroll report reduced risk-on appetite, pushing all 3 indexes at least 1% lower with tech stocks (excluding Nvidia) bearing the brunt of the downturn and as a result, the Nasdaq Composite Index as well. Powell’s testimony Wednesday and Thursday in which he stated the Fed may soon be in a position to cut rates helped push longer-term Treasury rates lower and stock indexes higher. Friday’s mixed payroll report, showing a larger-than-expected increase in jobs created but slower-than-expected wage growth and a higher-than-expected unemployment rate, ended up moving indexes lower to close the week lower. For the week, the S&P 500 Index decreased 0.3% to 5,123.69, the Nasdaq Composite Index fell 1.2% to 16,085.11, the Dow Jones Industrial Average lost 0.9% to close at 38,723.15, the 10-year U.S. Treasury rate fell 10bp to 4.08% and the U.S. dollar (as measured by the ICE U.S. Dollar index – DXY) weakened 1.1%.

Oil prices moved lower last week, falling every day but Wednesday. Increased China growth concerns, primarily due to lack of concrete stimulus measures combined with declining oil imports, greatly contributed to oil’s price decline. Wednesday’s move higher followed a much greater-than-expected decline in distillate and gasoline inventories and dovish Fed Chair Powell testimony.

Spot gold prices powered higher again last week driven by growing expectations of rate cuts as soon as June and by continued haven demand. Prices rose every day last week, at first in expectation of favorable Fed Chair Powell testimony and then following Powell testimony that the Fed will likely be in a position to lower rates soon. Friday’s employment report showing slowing wage growth and a higher unemployment rate also helped gold prices move higher.

Base metal prices moved higher as well last week benefiting from better-than-expected China trade data and a noticeably weaker U.S. dollar. Fed Chair Powell’s congressional testimony, affirming the possibility of rate cuts sooner than later, weakened the U.S. dollar and, as a result, boosted base metal prices. Copper prices were also supported by falling inventory levels and zinc prices were buoyed by reduced South Korea smelter production.

Grain prices, except for Chicago wheat prices, all moved higher last week. Corn prices seemingly moved higher on no real news, perhaps buoyed by short covering. Soybean prices benefited from better-than-expected exports and higher soybean oil and meal prices and wheat prices rose on decent export inspections and concerns regarding India crop production due to adverse weather forecasts/conditions. Chicago wheat prices declined due to China’s continued cancelation of orders.

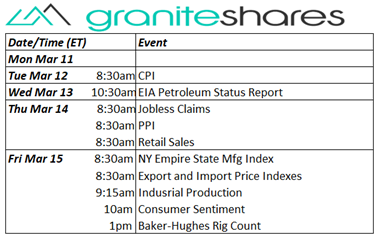

Coming Up This Week

Busy Friday but all eyes will be lifted toward Tuesday’s CPI release.

Busy Friday but all eyes will be lifted toward Tuesday’s CPI release.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.