Commodities & Precious Metals Weekly Report: Apr 30

Posted:

Key points

Energy prices were all higher last week. WTI and Brent crude oil prices rose about 2% and gasoline and natural gas prices increased over 3%.

Energy prices were all higher last week. WTI and Brent crude oil prices rose about 2% and gasoline and natural gas prices increased over 3%.- Grain prices were all higher as well. Wheat prices rose about 3 ¼ percent, corn prices increased almost 6.5% and soybean prices rose just over 1%. Soybean oil prices rose 6%.

- Base metal prices were all higher with nickel prices increasing the most. Nickel prices increased 8%, copper prices rose 3%, zinc prices rose 2.5% and aluminum prices increased 1%.

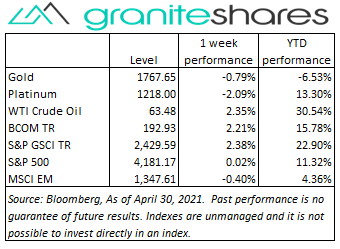

- Precious metal prices were all lower. Platinum prices fell 2.1%, silver prices lost 1% and gold prices decreased just under 1%.

- The Bloomberg Commodity Index increased another 2.2% last week. The energy and grains sectors were the primary contributors to performance followed by the base metals sector. The precious metals sector was the only sector with negative performance.

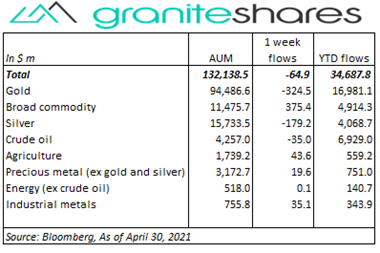

- Small net outflows last week but with the continued trend of gold and silver ETP outflows and broad commodity ETP inflows. Gold and silver ETPs saw outflows of about $325 million and $180 million, respectively. Broad commodity ETPs saw $375 million inflows.

Commentary

U.S. stock markets struggled last week though finished the month with strong gains. Alphabet, Amazon, Facebook, Apple and Microsoft all reported much better-than-expected earnings while consumer confidence and home prices posted outsized increases. The first estimate of Q1 GDP came in slightly below expectations but was still strong and personal income, savings and expenditures all showed better-than-expected gains. Fed Chairman Powell, following the FOMC’s decision to continue unchanged with its aggressively accommodative monetary policy, downplayed inflation concerns, saying inflation would likely rise in the near term but would dissipate in the coming months. The PCE price index, the Fed’s preferred inflation metric, increased 2.3% year-over-year, resulting both from increasing prices and subdued inflation numbers last March. Despite reaching record highs during the week, the S&P 500 and Nasdaq Composite Indexes were unchanged to slightly lower on the week. For the week, the S&P 500 Index was practically unchanged at 4,181.17, the Dow Jones Industrial Average decreased 0.5% to 33,874.85, the Nasdaq Composite Index decreased 0.4% to 13,962.68, the 10-year U.S. Treasury rate increased 6bps to 1.63% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) strengthened 0.5%.

U.S. stock markets struggled last week though finished the month with strong gains. Alphabet, Amazon, Facebook, Apple and Microsoft all reported much better-than-expected earnings while consumer confidence and home prices posted outsized increases. The first estimate of Q1 GDP came in slightly below expectations but was still strong and personal income, savings and expenditures all showed better-than-expected gains. Fed Chairman Powell, following the FOMC’s decision to continue unchanged with its aggressively accommodative monetary policy, downplayed inflation concerns, saying inflation would likely rise in the near term but would dissipate in the coming months. The PCE price index, the Fed’s preferred inflation metric, increased 2.3% year-over-year, resulting both from increasing prices and subdued inflation numbers last March. Despite reaching record highs during the week, the S&P 500 and Nasdaq Composite Indexes were unchanged to slightly lower on the week. For the week, the S&P 500 Index was practically unchanged at 4,181.17, the Dow Jones Industrial Average decreased 0.5% to 33,874.85, the Nasdaq Composite Index decreased 0.4% to 13,962.68, the 10-year U.S. Treasury rate increased 6bps to 1.63% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) strengthened 0.5%.

Oil prices moved higher last week supported by OPEC+ meeting a day earlier than planned and quickly agreeing to maintain their plans of increasing oil production gradually over the next 3 months. Prices were also supported by a much smaller-than-expected increase in U.S. oil reserves and a much larger-than-expected drawdown in distillate inventories. Oil prices fell Friday perhaps over increasing concerns regarding record Covid-19 infections in India and perhaps on profit-taking. Natural gas prices rose on continued strong export demand and forecasts of warmer-than-usual temperatures in the U.S. over the next two weeks.

Gold prices moved lower last week pressured by the combination of strong economic data and Fed Chairman Powell downplaying the risks of inflation. The FOMC, following the end of its 2-day meeting on Wednesday, left its aggressive accommodative monetary policy in place leaving its Fed Funds Rate target near 0% and continuing unabated with its Treasury and mortgage-backed securities buyback program. Silver prices followed gold prices while platinum prices took their cue from falling palladium prices.

Copper prices rose to 10-year highs last week propelled by Chilean port workers threatening to strike (Chile produces ¼ of the world’s copper supply). Continued expectations of increased copper demand due both to post-pandemic economic recovery and forecasted sustainable-energy demand also supported copper prices. Nickel prices moved sharply higher supported by growing demand expectations from EV production and sustainable-energy needs.

Grain prices continued to move higher last week benefiting from both strong Chinese demand and adverse weather conditions in the U.S. and abroad. Dry, drought like conditions in some of the U.S. Plains states drove wheat prices to 7-year highs last week while dry conditions in Brazil helped support corn and soybean prices.

Coming up this week

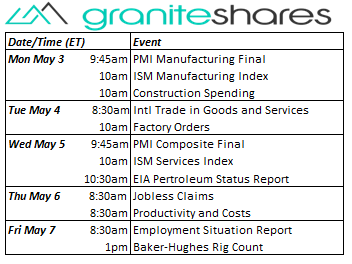

Data highlights for the week include PMI and ISM manufacturing and services indexes and the Employment Situation Report on Friday.

Data highlights for the week include PMI and ISM manufacturing and services indexes and the Employment Situation Report on Friday.- PMI and ISM Manufacturing Indexes and Construction Spending on Monday.

- International Trade in Goods and Services and Factory Orders on Tuesday.

- PMI Composite and ISM Services Indexes on Wednesday.

- Jobless Claims and Productivity and Costs on Thursday.

- Employment Situation Report on Friday.

- EIA petroleum status report on Wednesday and Baker-Hughes rig count on Friday.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.