Commodities & Precious Metals Weekly Report: Dec 08

Posted:

Key points

Energy prices moved lower again. WTI and Brent crude oil prices fell 4%, heating oil and gasoline prices dropped 3% and natural gas prices fell 8%.

Energy prices moved lower again. WTI and Brent crude oil prices fell 4%, heating oil and gasoline prices dropped 3% and natural gas prices fell 8%.- Grain prices were mixed. Wheat prices rose between 2% and 5% and corn prices were marginally higher. Soybean, soybean meal and soybean oil prices fell 2 percent.

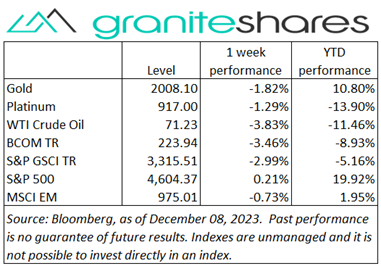

- Spot gold prices fell 3%, spot silver prices dropped 10% and platinum prices decreased 1%.

- Base metal prices were all lower. Lead and zinc prices lost 5%, aluminum prices dropped 4%, copper prices fell 3% and nickel prices decreased 2%.

- The Bloomberg Commodity Index decreased 3.5%. All sectors were down on the week with the energy and precious and base metals sectors comprising most of the losses.

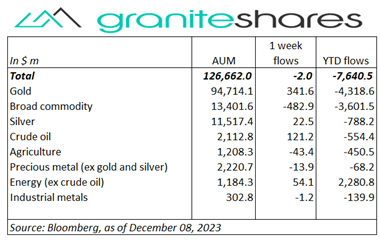

- Practically zero net flows last week with large broad commodity ETP outflows offset by decent gold and and energy ETP inflows.

Commentary

While stock markets mainly moved higher last week, gains were relatively muted. The Nasdaq Composite Index outperformed the S&P 500 Index and the Dow Jones Industrial Average, benefiting from increased AI interest and expectations as well as from continued expectations of Fed rate cuts beginning next year. A resilient U.S. economy (illustrated by a stronger-than-expected payroll report and improving consumer sentiment) along with tempering inflation seems to have supported hopes for a “soft-landing” while at the same time increasing uncertainty regarding future Fed monetary policy and longer-term rate levels. The 10-year Treasury rate, for example, ended the week almost unchanged after falling 10bps through Wednesday. For the week, the S&P 500 Index increased 0.2% to 4,604.37, the Nasdaq Composite Index rose 0.8% to 14,403.97, the Dow Jones Industrial Average was practically unchanged at 36,247.74, the 10-year U.S. Treasury rate increased 2bps to 4.23% and the U.S. dollar (as measured by the ICE U.S. Dollar index – DXY) strengthened 0.7%.

While stock markets mainly moved higher last week, gains were relatively muted. The Nasdaq Composite Index outperformed the S&P 500 Index and the Dow Jones Industrial Average, benefiting from increased AI interest and expectations as well as from continued expectations of Fed rate cuts beginning next year. A resilient U.S. economy (illustrated by a stronger-than-expected payroll report and improving consumer sentiment) along with tempering inflation seems to have supported hopes for a “soft-landing” while at the same time increasing uncertainty regarding future Fed monetary policy and longer-term rate levels. The 10-year Treasury rate, for example, ended the week almost unchanged after falling 10bps through Wednesday. For the week, the S&P 500 Index increased 0.2% to 4,604.37, the Nasdaq Composite Index rose 0.8% to 14,403.97, the Dow Jones Industrial Average was practically unchanged at 36,247.74, the 10-year U.S. Treasury rate increased 2bps to 4.23% and the U.S. dollar (as measured by the ICE U.S. Dollar index – DXY) strengthened 0.7%.

Oil prices moved lower last week, affected by both demand and supply concerns. Prices continued to react negatively to last week's OPEC+ announcement calling for increased but voluntary production cutbacks and to increased global demand concerns. Wednesday’s EIA release showing a much larger-than-expected build in gasoline stocks particularly unsettled markets, pushing WTI crude oil prices over 4% lower. Friday’s stronger-than-expected jobs report and Saudi Arabia’s and Russia’s entreaty to other OPEC+ members to reduce production lifted prices about 3% higher, moving prices off of Thursday’s lows. Natural gas prices fell 8%, reacting to warm-weather forecasts, increased production and high inventory levels.

Gold prices gave up some of their gains last week, falling pronouncedly on Monday and Friday. Lower on Monday due to renewed uncertainty regarding the timing and extent of Fed rate cuts, prices remained relatively unchanged through Thursday. Friday’s stronger-than-expected jobs report pushed prices lower, again on increased uncertainty surrounding Fed monetary policy going forward. Silver and platinum prices also fell, with silver significantly underperforming gold prices and platinum prices outperforming gold prices.

Copper prices moved lower last week as well. Concerns regarding Chinese demand (due to stimulus implementation doubts and Moody’s outlook downgrade), a stronger U.S. dollar and a recent increase in inventories, all contributed to lower prices. Copper prices moved higher Thursday and Friday (off of mid-week lows), benefiting from better-than-expected Chinese export data and a stronger-than-expected U.S. jobs report.

Wheat was the best performer last week with prices supported by strong exports (particularly to China) and lowered Argentina production estimates. Prices fell almost 2% Friday, though, following WASDE’s smaller-than-expected reduction in ending stocks. Corn prices, ending the weak marginally higher, benefited from strong exports (more competitive pricing versus Brazil and Argentina) but suffered from WASDE’s (released Friday) larger-than-expected estimates of Brazil and Argentina production. Soybean prices fell on improved weather forecasts for Brazil and Argentina and lower oil prices.

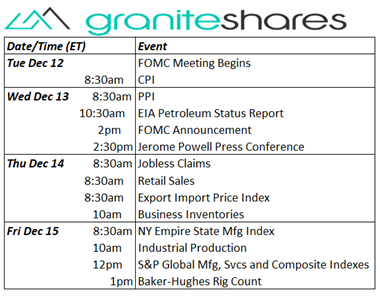

Coming Up This Week

CPI (Tuesday) and FOMC Decision (Wednesday) take center stage this week. Retail Sales and PMI Indexes also of interest.

CPI (Tuesday) and FOMC Decision (Wednesday) take center stage this week. Retail Sales and PMI Indexes also of interest.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.