Commodities & Precious Metals Weekly Report: Dec 10

Posted:

Key points

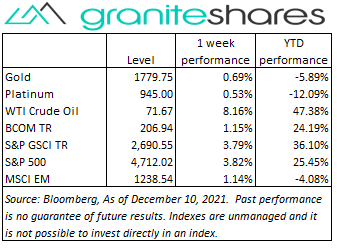

Except for natural gas prices, energy prices were all higher last week. WTI and Brent crude oil prices rose approximately 8%, gasoline prices increased 9.5% and heating oil prices rose almost 7.5%. Natural gas prices fell 5%.

Except for natural gas prices, energy prices were all higher last week. WTI and Brent crude oil prices rose approximately 8%, gasoline prices increased 9.5% and heating oil prices rose almost 7.5%. Natural gas prices fell 5%.- Grain prices were mixed with wheat prices falling, corn prices rising and soybean prices unchanged. Kansas and Chicago wheat prices fell 2 ¼ percent. Corn prices increased 1%.

- Precious metal prices were mixed as well. February gold futures prices were practically unchanged and February silver futures prices were down 1.2%. Platinum prices increased ½ percent.

- Base metal prices were mixed, too. Aluminum and nickel prices fell 0.8% and 1.5%, respectively. Copper and zinc prices increased 0.5% and 5.4%, respectively.

- The Bloomberg Commodity Index gained 1.2% percent benefiting primarily from higher energy prices. The base metals sector was the only other positive performing sector.

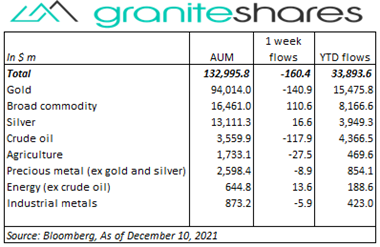

- Small commodity ETP outflows (-$160m) last week. Gold (-$141m) and crude oil (-$118) outflows were partially offset by broad commodity ($111m) inflows.

Commentary

A strong week for U.S. stock markets with all three major indexes increasing north of 3.5% and the S&P 500 Index finishing the week at a record high. Stock markets rose sharply Monday and Tuesday, rallying in relief to positive news regarding the seriousness of the omicron variant and the effectiveness of existing vaccines against it. Thursday was the only down day for stock markets perhaps due to investor trepidation before Friday’s CPI release and despite lower-than-expected jobless claims. Friday’s 40-year-high CPI release, coming in slightly above expectations, moved stock markets even higher as investor concerns of “even higher inflation” and a much more aggressive Fed were allayed. The 10-year U.S. Treasury rate also moved higher on the week but closed off its intraweek high reached Wednesday. Most of the increase in the 10-year Treasury rate was due to rising real rates though inflation expectations also moved higher. For the week, the S&P 500 Index increased 3.8% to 4,712.02, the Nasdaq Composite Index rose 3.6% to 15,630.60, the Dow Jones Industrial Average gained 4.0% to 35,971.98, the 10-year U.S. Treasury rate increased 12bps to 1.48% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) was practically unchanged.

A strong week for U.S. stock markets with all three major indexes increasing north of 3.5% and the S&P 500 Index finishing the week at a record high. Stock markets rose sharply Monday and Tuesday, rallying in relief to positive news regarding the seriousness of the omicron variant and the effectiveness of existing vaccines against it. Thursday was the only down day for stock markets perhaps due to investor trepidation before Friday’s CPI release and despite lower-than-expected jobless claims. Friday’s 40-year-high CPI release, coming in slightly above expectations, moved stock markets even higher as investor concerns of “even higher inflation” and a much more aggressive Fed were allayed. The 10-year U.S. Treasury rate also moved higher on the week but closed off its intraweek high reached Wednesday. Most of the increase in the 10-year Treasury rate was due to rising real rates though inflation expectations also moved higher. For the week, the S&P 500 Index increased 3.8% to 4,712.02, the Nasdaq Composite Index rose 3.6% to 15,630.60, the Dow Jones Industrial Average gained 4.0% to 35,971.98, the 10-year U.S. Treasury rate increased 12bps to 1.48% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) was practically unchanged.

Oil also moved higher last week mainly benefiting from a relief rally tied to lessened concerns regarding the seriousness of the Omicron Covid variant, reduced Fed tightening concerns and, to a lesser extent, setbacks in Iran nuclear agreement negotiations. Oil price increases were capped by China demand concerns – precipitated by ratings downgrades of Evergrande and Kaisa groups – and a smaller-than-expected fall in U.S. oil inventories. Natural gas prices moved sharply lower Monday, falling over 11% on continued warm weather forecasts, though prices moved higher the remainder of the week as weather models flipped, forecasting colder weather for last two weeks of December.

Gold edged higher last week, maintaining levels even as the U.S. dollar strengthened and 10-year U.S. real rates moved higher. Down about ½ percent through Thursday, gold prices increased about ½ percent Friday following the 40-year-high CPI release perhaps due to investor expectations of an even worse release, ameliorating concerns of a much more aggressive Fed (with respect to tightening monetary policy). Despite lessening concerns regarding the severity of the Omicron Covid variant, announcements of new precautionary, Covid-related restrictions in the UK and Europe increased expectations of slower growth and continued central bank easy money policies helping to support gold prices as well.

Buoyed by increased Chinese imports, the PBoC’s lowering of reserve requirements and lessening concerns surrounding the economic impact of the Omicron Covid variant, copper prices increased nearly 3% through Wednesday. Announcements of precautionary Omicron-related restrictions in Europe and the UK and the ratings downgrade of Chinese property firms Evergrande and Kaisa moved copper prices lower the remainder of the week, leaving copper prices up about ½ percent for the week. Zinc prices, up over 5% last week, moved higher on Glencore’s “maintainance and care” shutdown of Its smelter in Italy. The shutdown prompted supply concerns, driving prices higher.

Slightly higher through Tuesday, wheat prices fell almost 4% over Wednesday and Thursday pressured by favorable weather forecasts in the U.S. Plain states and larger-than-expected U.S. and global ending inventories as released in Thursday’s USDA WASDE report. Corn prices were supported by growing ethanol demand (despite new, lower U.S government ethanol requirements in gasoline), higher oil prices and by concerns of a possible Russian invasion of corn-producing Ukraine. Soybean prices were volatile last week, influenced by expectations of a large South American crop and weak demand from China.

Coming up this week

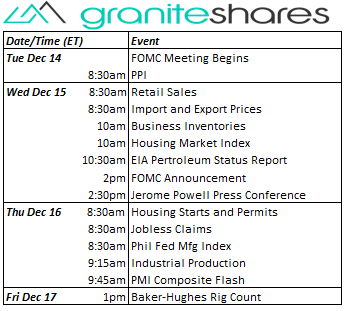

Busy data week with the 2-day FOMC meeting (beginning Tuesday) dominating the week.

Busy data week with the 2-day FOMC meeting (beginning Tuesday) dominating the week.- FOMC meeting begins and PPI on Tuesday.

- Import and Export Prics, Business Inventories, Housing Market Index and FOMC announcement and Jerome Powell Press Conference on Wednesday.

- Housing Starts and Permits, Jobless Claims, Phil Fed Mfg Index, Industrial Production and PMI Composite Flash on Thursday.

- EIA Petroleum Status Report Wednesday and Baker-Hughes Rig Count on Friday.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.