Commodities & Precious Metals Weekly Report: Dec 22

Posted:

Key points

Energy prices were higher last week. WTI and Brent crude oil prices and gasoil prices increased between 2% and 3% and heating oil prices rose 1%. Gasoline and natural gas prices were basically unchanged.

Energy prices were higher last week. WTI and Brent crude oil prices and gasoil prices increased between 2% and 3% and heating oil prices rose 1%. Gasoline and natural gas prices were basically unchanged.- Grain prices were mixed. Wheat prices fell between 2% and 3% and corn and soybean prices lost 2%.

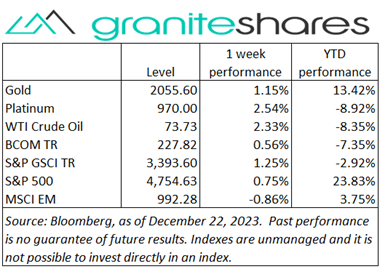

- Spot gold and silver prices increased 2% and spot platinum prices rose 4%. Palladium prices increased 3%.

- Base metal prices were all mixed. Aluminum and zinc prices rose 3% and copper prices gained less than ½ percent. Nickel prices fell 4% and lead prices decreased 1%.

- The Bloomberg Commodity Index increased 0.6%, benefiting primarily from gains in the energy and precious metals sectors. Gains were offset mainly by grains sector losses.

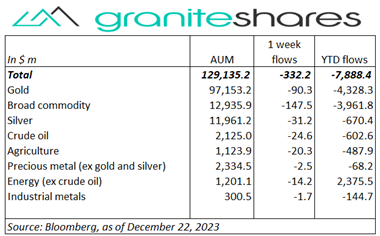

- Outflows from all sectors led by broad commodity and then gold ETPs.

Commentary

Another positive week for stock markets with all 3 major indexes moving higher. Indexes recorded gains each day last week, except for Wednesday when they experienced sharp declines Momentum from last week’s gains moved indexes higher early in the weak, driven by expectations of early-next-year rate cuts combined with a resilient economy, despite some hawkish comments by Fed officials. Wednesday’s sharp sell-off (with all 3 indexes dropping at least 1 ¼ percent) came on the heels of stronger-than-expected consumer confidence and existing home sales, seemingly tempering rate cut expectations and, as a result, bolstering risk-off sentiment. Those concerns, however, significantly faded with Thursday’s revised-lower Q3 GDP (final estimate) and, perhaps more importantly, with Thursday’s revised-lower third quarter PCE Price Index (part of the GDP report). Friday’s better-than-expected current PCE Price Index release reduced concerns further, supporting stock prices. For the week, the S&P 500 Index rose 0.8% to 4,754.63, the Nasdaq Composite Index climbed 1.2% to 14,992.97, the Dow Jones Industrial Average increased 0.2% to 37,385.97, the 10-year U.S. Treasury rate fell 1bps to 3.90% and the U.S. dollar (as measured by the ICE U.S. Dollar index – DXY) weakened 0.9%.

Another positive week for stock markets with all 3 major indexes moving higher. Indexes recorded gains each day last week, except for Wednesday when they experienced sharp declines Momentum from last week’s gains moved indexes higher early in the weak, driven by expectations of early-next-year rate cuts combined with a resilient economy, despite some hawkish comments by Fed officials. Wednesday’s sharp sell-off (with all 3 indexes dropping at least 1 ¼ percent) came on the heels of stronger-than-expected consumer confidence and existing home sales, seemingly tempering rate cut expectations and, as a result, bolstering risk-off sentiment. Those concerns, however, significantly faded with Thursday’s revised-lower Q3 GDP (final estimate) and, perhaps more importantly, with Thursday’s revised-lower third quarter PCE Price Index (part of the GDP report). Friday’s better-than-expected current PCE Price Index release reduced concerns further, supporting stock prices. For the week, the S&P 500 Index rose 0.8% to 4,754.63, the Nasdaq Composite Index climbed 1.2% to 14,992.97, the Dow Jones Industrial Average increased 0.2% to 37,385.97, the 10-year U.S. Treasury rate fell 1bps to 3.90% and the U.S. dollar (as measured by the ICE U.S. Dollar index – DXY) weakened 0.9%.

Oil prices rose last week powered primarily by a combination of good economic data (lower-than-expected U.S., UK and euro zone inflation) and by Houthi attacks on Red Sea tankers. The formation of a task force to address Red Sea attacks and Angola’s intent to leave OPEC moved prices lower Thursday and Friday, off Wednesday’s highs.

Gold prices moved lockstep to stock prices, rising early in the week, retracting Wednesday, and then rising the remainder of the week. Underlying forces were similar as well, with continued Fed rate-cut, cooling inflation and resilient economy expectations responsible for price gains early in the week. Doubts of those same expectations moved prices lower Wednesday only to see them rebound and more Thursday and Friday following a revised-lower Q3 GDP and a better-than-expected PCE Price Index release. Silver prices moved with gold prices while platinum prices outperformed.

Copper prices moved higher last week, overcoming Chinese property market concerns and benefiting from much stronger-than expected November Chinese copper imports. Prices were also supported by mining disruptions and a weaker U.S. dollar. Aluminum prices moved higher on the week, moving off intraweek lows reached on growing inventory levels. Potential supply disruptions due to an oil terminal explosion in Guinea pushed prices sharply higher Friday. Nickel prices, lower on the week, continue to suffer from oversupply concerns.

A down week for grain prices. Corn and soybean prices moved lower on improved South American and U.S. weather forecasts, continued closure of Mexico border passes and cheaper Brazil prices. Wheat prices also suffered from improved weather forecasts but also from cheap Russian exports.

Coming Up This Week

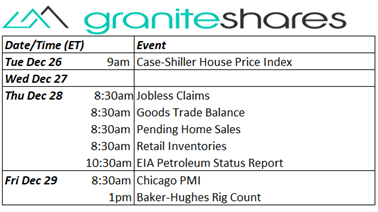

Light data-week with releases concentrated on Thursday.

Light data-week with releases concentrated on Thursday.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.