Commodities & Precious Metals Weekly Report: Dec 23

Posted:

Key points

Energy prices were mainly higher last week. WTI and Brent crude oil and gasoline prices increased about 4 ¼ percent. Heating oil prices rose almost 4 ¾ percent. Natural gas prices moved slightly lower, falling about ½ percent.

Energy prices were mainly higher last week. WTI and Brent crude oil and gasoline prices increased about 4 ¼ percent. Heating oil prices rose almost 4 ¾ percent. Natural gas prices moved slightly lower, falling about ½ percent. - Grain prices were all higher. Chicago and Kansas wheat prices increased 5.1% and 6.4%, respectively. Corn and soybean prices increased 2.1% and 4.1%, respectively.

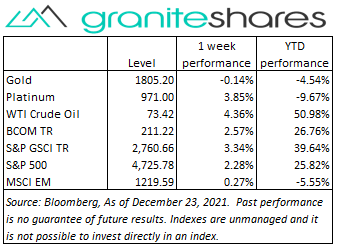

- Precious metal prices were all higher as well. February gold and silver futures prices increased 0.4% and 1.8%, respectively. Platinum prices increased just under 4%.

- Base metal prices, too, were higher. Aluminum prices increased another 4.5% and zinc prices rose 4.4%. Copper prices increased 2.3% and nickel prices gained 1.9%.

- The Bloomberg Commodity Index rose 2.6%, primarily due to positive performances in the energy, grains and base metals sectors.

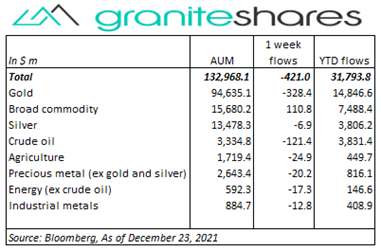

- $421 million commodity ETP outflows with gold (-$328m) and crude oil (-$121m) outflows partially offset by broad commodity ($11m) inflows. Smaller outflows in the remaining sectors.

Commentary

After falling over 1% Monday, all three major stock indexes rallied the remainder of the holiday-shortened week to finish sharply higher and with the S&P 500 Index closing at a record high. Waning Omicron fears (spurred by reports of booster effectiveness, approval of Pfizer’s Covid pill and the mildness of Omicron cases) were the primary reason for last week’s gains with markets relief-rallying after 3 days of significant declines. Tech stocks reversed the previous week’s underperformance with the Nasdaq Composite Index markedly outperforming both the Dow Jones Industrial Average and the S&P 500 Index. The 10-year U.S. Treasury rate mirrored stock market performances, falling Monday and then rising through Friday to finish just below 1.5% while the U.S. dollar weakened as investors resumed risk-on investing. For the week, the S&P 500 Index increased 2.3% to 4,725.78, the Nasdaq Composite Index rose 3.2% to 15,653.37, the Dow Jones Industrial Average increased 1.7% to 35,950.63, the 10-year U.S. Treasury rate increased 8bps to 1.49% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) weakened 0.6%.

After falling over 1% Monday, all three major stock indexes rallied the remainder of the holiday-shortened week to finish sharply higher and with the S&P 500 Index closing at a record high. Waning Omicron fears (spurred by reports of booster effectiveness, approval of Pfizer’s Covid pill and the mildness of Omicron cases) were the primary reason for last week’s gains with markets relief-rallying after 3 days of significant declines. Tech stocks reversed the previous week’s underperformance with the Nasdaq Composite Index markedly outperforming both the Dow Jones Industrial Average and the S&P 500 Index. The 10-year U.S. Treasury rate mirrored stock market performances, falling Monday and then rising through Friday to finish just below 1.5% while the U.S. dollar weakened as investors resumed risk-on investing. For the week, the S&P 500 Index increased 2.3% to 4,725.78, the Nasdaq Composite Index rose 3.2% to 15,653.37, the Dow Jones Industrial Average increased 1.7% to 35,950.63, the 10-year U.S. Treasury rate increased 8bps to 1.49% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) weakened 0.6%.

Oil prices moved similarly to equity markets, moving lower Monday and then rallying the remainder of the week. As with equity markets, lessening Omicron fears, brought about by reports of booster effectiveness and the mildness of Omicron cases, buoyed oil prices, precipitating a relief rally. Wednesday’s EIA reports showing a much larger-than-expected decline in U.S. oil inventories also supported prices.

After falling Monday and Tuesday, gold prices moved higher over Wednesday and Thursday despite lessening Omicron concerns. February futures prices moved ¾ percent higher Wednesday most likely boosted by a weakening U.S. dollar as investors resumed risk-on trading. 10-year U.S. real yields also supported gold prices, maintaining historically low and negative levels.

Base metal prices moved higher as well last week supported both by continued supply concerns, low inventories and reduced Omicron-related concerns. Continued zinc and aluminum production concerns resulting from soaring energy costs, boosted prices with both zinc and aluminum prices moving 4.5% higher through Thursday.

Grain prices moved higher last week benefiting in general from the resumption of risk-on trading and a weaker U.S. dollar. Corn and soybean prices were also supported by dry-weather concerns primarily in Brazil but also in Argentina. Corn prices also benefited from rising oil prices (ethanol related). Wheat prices moved higher on supply concerns with Russia limiting exports through excise taxes, Ukraine considering limiting exports and weather concerns potentially affecting Australian high-quality wheat harvests.

Coming up this week

Very light week with most data, again, released Wednesday and Thursday.

Very light week with most data, again, released Wednesday and Thursday.- Case-Shiller Home Price Index on Tuesday.

- Intl Trade in Goods and Pending Home Sales Index on Wednesday.

- Jobless Claims and Chicago PMI on Thursday.

- EIA Petroleum Status Report Wednesday and Baker-Hughes Rig Count on Thursday.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.