Commodities & Precious Metals Weekly Report: Feb 4

Posted:

Key points

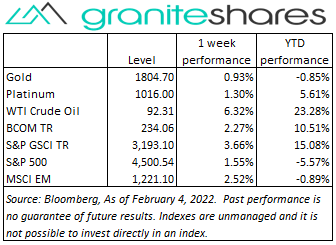

Energy prices, except for natural gas prices, moved higher last week. WTI and Brent crude oil prices increased 6.3% and 5.1%, respectively, gasoline prices rose 5% and heating oil prices increased 6.0%. Natural gas prices fell 1.4%.

Energy prices, except for natural gas prices, moved higher last week. WTI and Brent crude oil prices increased 6.3% and 5.1%, respectively, gasoline prices rose 5% and heating oil prices increased 6.0%. Natural gas prices fell 1.4%. - Grain prices were mixed. Chicago and Kansas wheat prices fell 2.9% and 2.1%, respectively and corn prices lost 2.4%. Soybean prices climbed 5.7%.

- Precious metal prices increased. Gold and silver prices increased just under 1%. Platinum prices rose 1.3%

- Base metal prices were mixed as well. Copper and nickel prices rose 4.1% and 3.1%, respectively, while aluminum and zinc prices edged lower, falling 0.3% and 0.2%, respectively.

- The Bloomberg Commodity Index rose 1.3% with half the gain coming from the energy sector. All sectors of the index had positive performance.

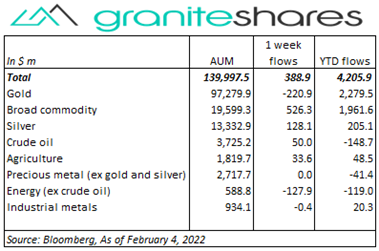

- Commodity ETPs experienced net inflows ($389m) last week with strong inflows into broad commodity ($526m) and silver ($128m) ETPs partially offset by outflows from gold (-$221m) and energy (ex-crude oil) (-$128) ETPs.

Commentary

U.S. stock markets rallied strongly through Wednesday, buoyed by strong tech-stock earnings, with the Nasdaq Composite Index climbing just under 5%. Wednesday’s after-market Meta Platforms earnings report all but reversed those gains Thursday, with Meta’s stock price plunging 26% and driving the Nasdaq Composite Index 3.7% lower. Those losses, in turn, were partially reversed Friday following Amazon’s after-market earnings report Thursday, with Amazon’s stock price surging just under 14% and the Nasdaq Composite Index increasing 1.6%. Friday’s much stronger-than-expected Non-Farm Payroll Report, along with the BoE’s rate increase Thursday and growing expectations the ECB will tighten monetary policy, drove 10-year U.S. Treasury rates 14bps higher to finish the week above 1.9%. The U.S. dollar, however, weakened significantly over the week, partly as result of the BoE tightening actions. The Nasdaq Composite Index outperformed both the S&P 500 Index and the Dow Jones Industrial Average as investors favored growth/tech stocks over value/cyclical stocks. At week’s end, the S&P 500 Index gained 1.6% to 4,500.54, the Nasdaq Composite Index rose 2.4% to 14,098.01, the Dow Jones Industrial Average increased 0.7% to 35,089.15, the 10-year U.S. Treasury rate rose 14bp to 1.92% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) weakened 1.8%.

U.S. stock markets rallied strongly through Wednesday, buoyed by strong tech-stock earnings, with the Nasdaq Composite Index climbing just under 5%. Wednesday’s after-market Meta Platforms earnings report all but reversed those gains Thursday, with Meta’s stock price plunging 26% and driving the Nasdaq Composite Index 3.7% lower. Those losses, in turn, were partially reversed Friday following Amazon’s after-market earnings report Thursday, with Amazon’s stock price surging just under 14% and the Nasdaq Composite Index increasing 1.6%. Friday’s much stronger-than-expected Non-Farm Payroll Report, along with the BoE’s rate increase Thursday and growing expectations the ECB will tighten monetary policy, drove 10-year U.S. Treasury rates 14bps higher to finish the week above 1.9%. The U.S. dollar, however, weakened significantly over the week, partly as result of the BoE tightening actions. The Nasdaq Composite Index outperformed both the S&P 500 Index and the Dow Jones Industrial Average as investors favored growth/tech stocks over value/cyclical stocks. At week’s end, the S&P 500 Index gained 1.6% to 4,500.54, the Nasdaq Composite Index rose 2.4% to 14,098.01, the Dow Jones Industrial Average increased 0.7% to 35,089.15, the 10-year U.S. Treasury rate rose 14bp to 1.92% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) weakened 1.8%.

Oil prices continued to rise last week with WTI crude oil prices surpassing 7-year highs and closing above $90/barrel. Tight supplies brought about by moderate OPEC+ production increases (worsened by production setbacks in a number of OPEC+ member states), a larger-than-expected decline in U.S. oil Inventories, Middle East tensions (Houthi missile fired at Abu Dhabi) and continued U.S.-Russia tensions over Ukraine continued to support oil prices. Forecasts of frigid weather in the U.S. and particularly in Texas pressured oil prices 4% higher over Thursday and Friday with increased concerns of weather-related production/refining shutdowns.

Gold prices moved higher last week, supported mainly by a weaker U.S. dollar and U.S.-Russia tensions surrounding Ukraine. A much weaker-than-expected ISM Manufacturing Index released Monday lowered expectations of aggressive Fed tightening, sharply weakening the U.S. dollar and moving 10-year real yields slightly lower, both supporting gold prices. 10-year real yields moved higher the remainder of the week, increasing 19bps to -50bps, with 15bps of that move occurring over Thursday and Friday as the BoE’s rate increase Thursday and a much stronger-than-expected employment report Friday increased expectations of more rather than less Fed action. Gold prices, nonetheless, maintained price levels with growing concerns of unwanted higher-than-expected inflation (the 10-year breakeven rate closed the week at 2.41%, down only 5bps).

Base metal prices were mixed last week with copper and nickel prices rising and aluminum and zinc prices falling slightly. Light trading volume due to the Chinese Lunar New Year holiday and a sharply weaker U.S. dollar helped move copper and nickel prices higher. Aluminum prices, up nearly 8% in January because of production cutbacks due to soaring energy costs, were very volatile last week moving almost +/-2% Monday, Wednesday and Thursday.

Grain prices were were mixed last week with wheat and corn prices falling and soybean prices rising. Soybean prices rose on hot, dry weather in South America (lowering harvest expectations) and strong demand. Wheat prices, up over the last few weeks on Russia-Ukraine tensions, consolidated with no change to the situation and no disruption to wheat exports.

U.S. stock markets rallied strongly through Wednesday, buoyed by strong tech-stock earnings, with the Nasdaq Composite Index climbing just under 5%. Wednesday’s after-market Meta Platforms earnings report all but reversed those gains Thursday, with Meta’s stock price plunging 26% and driving the Nasdaq Composite Index 3.7% lower. Those losses, in turn, were partially reversed Friday following Amazon’s after-market earnings report Thursday, with Amazon’s stock price surging just under 14% and the Nasdaq Composite Index increasing 1.6%. Friday’s much stronger-than-expected Non-Farm Payroll Report, along with the BoE’s rate increase Thursday and growing expectations the ECB will tighten monetary policy, drove 10-year U.S. Treasury rates 14bps higher to finish the week above 1.9%. The U.S. dollar, however, weakened significantly over the week, partly as result of the BoE tightening actions. The Nasdaq Composite Index outperformed both the S&P 500 Index and the Dow Jones Industrial Average as investors favored growth/tech stocks over value/cyclical stocks. At week’s end, the S&P 500 Index gained 1.6% to 4,500.54, the Nasdaq Composite Index rose 2.4% to 14,098.01, the Dow Jones Industrial Average increased 0.7% to 35,089.15, the 10-year U.S. Treasury rate rose 14bp to 1.92% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) weakened 1.8%.

Oil prices continued to rise last week with WTI crude oil prices surpassing 7-year highs and closing above $90/barrel. Tight supplies brought about by moderate OPEC+ production increases (worsened by production setbacks in a number of OPEC+ member states), a larger-than-expected decline in U.S. oil Inventories, Middle East tensions (Houthi missile fired at Abu Dhabi) and continued U.S.-Russia tensions over Ukraine continued to support oil prices. Forecasts of frigid weather in the U.S. and particularly in Texas pressured oil prices 4% higher over Thursday and Friday with increased concerns of weather-related production/refining shutdowns.

Gold prices moved higher last week, supported mainly by a weaker U.S. dollar and U.S.-Russia tensions surrounding Ukraine. A much weaker-than-expected ISM Manufacturing Index released Monday lowered expectations of aggressive Fed tightening, sharply weakening the U.S. dollar and moving 10-year real yields slightly lower, both supporting gold prices. 10-year real yields moved higher the remainder of the week, increasing 19bps to -50bps, with 15bps of that move occurring over Thursday and Friday as the BoE’s rate increase Thursday and a much stronger-than-expected employment report Friday increased expectations of more rather than less Fed action. Gold prices, nonetheless, maintained price levels with growing concerns of unwanted higher-than-expected inflation (the 10-year breakeven rate closed the week at 2.41%, down only 5bps).

Base metal prices were mixed last week with copper and nickel prices rising and aluminum and zinc prices falling slightly. Light trading volume due to the Chinese Lunar New Year holiday and a sharply weaker U.S. dollar helped move copper and nickel prices higher. Aluminum prices, up nearly 8% in January because of production cutbacks due to soaring energy costs, were very volatile last week moving almost +/-2% Monday, Wednesday and Thursday.

Grain prices were were mixed last week with wheat and corn prices falling and soybean prices rising. Soybean prices rose on hot, dry weather in South America (lowering harvest expectations) and strong demand. Wheat prices, up over the last few weeks on Russia-Ukraine tensions, consolidated with no change to the situation and no disruption to wheat exports.

Coming up this week

Very light data-week with CPI Thursday and Consumer Sentiment Friday.

Very light data-week with CPI Thursday and Consumer Sentiment Friday.- International Trade in Goods on Tuesday.

- Jobless Claims and CPI on Thursday.

- Consumer Sentiment on Friday.

- EIA Petroleum Status Report Wednesday and Baker-Hughes Rig Count on Friday.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.