Commoditized Wisdom: Report (Week Ending January 12, 2024)

Posted:

Key points

Energy prices were mixed. WTI and Brent crude oil prices fell 1%. Gasoline prices rose 1% and heating oil and gasoil prices increased 2%. Natural gas prices rose less than ¼ percent.

Energy prices were mixed. WTI and Brent crude oil prices fell 1%. Gasoline prices rose 1% and heating oil and gasoil prices increased 2%. Natural gas prices rose less than ¼ percent.- Grain prices were all lower. Wheat, corn and soybean prices fell 3%.

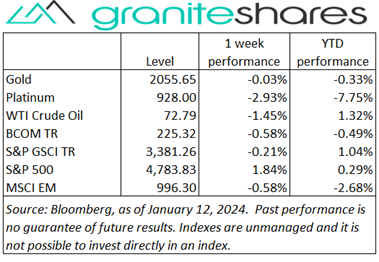

- Spot gold and silver prices rose 0.2%. Spot platinum and palladium prices fell 5%.

- Base metal prices, except for lead prices, were lower as well. Aluminum, copper and zinc prices fell between 2% and 3%. Nickel prices fell ½ percent. Lead prices rose 1%.

- The Bloomberg Commodity Index fell 0.6% mainly due to losses in the grains and base metals sectors.

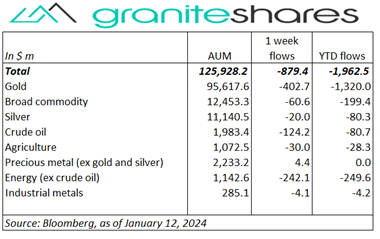

- More outflows again predominantly from gold ETPs but also from energy ETPs.

Commentary

All 3 major stock indexes moved higher last week but with a pronounced tilt in favor of the Nasdaq Composite Index. Stock prices moved markedly higher Monday, apparently rebounding off the previous week’s sharp decline and perhaps as a result of positioning in front of Thursday’s CPI release. Stock prices mainly moved higher over Tuesday and Wednesday, again on no real news and seemingly as positioning in front of Thursday’s CPI release. Thursday’s higher-than-expected CPI release, initially moving stock prices lower, ended up having little effect with all 3 major indexes finishing the day practically unchanged. Friday’s lower-than-expected PPI release helped support stock prices but a selection of weaker-than-expected earnings reports capped gains, pressuring stock prices lower. For the week, the S&P 500 Index rose 1.8% to 4,783.83, the Nasdaq Composite Index gained 3.1% to 14,972.76, the Dow Jones Industrial Average increased 0.3% to 37,593.24, the 10-year U.S. Treasury rate dropped 10bps to 3.95% and the U.S. dollar (as measured by the ICE U.S. Dollar index – DXY) was basically unchanged.

All 3 major stock indexes moved higher last week but with a pronounced tilt in favor of the Nasdaq Composite Index. Stock prices moved markedly higher Monday, apparently rebounding off the previous week’s sharp decline and perhaps as a result of positioning in front of Thursday’s CPI release. Stock prices mainly moved higher over Tuesday and Wednesday, again on no real news and seemingly as positioning in front of Thursday’s CPI release. Thursday’s higher-than-expected CPI release, initially moving stock prices lower, ended up having little effect with all 3 major indexes finishing the day practically unchanged. Friday’s lower-than-expected PPI release helped support stock prices but a selection of weaker-than-expected earnings reports capped gains, pressuring stock prices lower. For the week, the S&P 500 Index rose 1.8% to 4,783.83, the Nasdaq Composite Index gained 3.1% to 14,972.76, the Dow Jones Industrial Average increased 0.3% to 37,593.24, the 10-year U.S. Treasury rate dropped 10bps to 3.95% and the U.S. dollar (as measured by the ICE U.S. Dollar index – DXY) was basically unchanged.

Another volatile week with oil prices finishing about 1% lower. Oil prices moved sharply lower Monday, reacting to increased supplies from some OPEC producers as well as other non-OPEC producers. Prices moved higher Tuesday on increased Red Sea tensions but then fell sharply Wednesday after a surprise large build in U.S. inventories and on increased euro zone demand concerns. Thursday and Friday saw prices rise, bolstered by U.S. extreme cold weather forecasts, U.S. and British attacks on Houthi (Yemen) military sites and on Iran’s seizure of a freighter.

Spot gold prices ended the week slightly higher, recovering from an intraweek low of down over 1% set Wednesday. Less sanguine rate-cut expectations pressured spot prices lower through Wednesday in front of Thursday’s CPI release. A higher-than-expected CPI release, initially driving spot gold prices lower, was offset by increased Middle East concerns with prices finishing the day slightly higher. Growing Middle East concerns combined with a lower-than-expected PPI release moved spot gold prices over 1% higher Friday.

Copper prices ended the week lower mainly due to increased Chinese demand/economic health concerns and a higher-than-expected CPI release Thursday. Weakish Chinese M2 money supply and new loan data and smaller-than-expected BoC liquidity and credit provisions, increased Chinese demand growth concerns while uncertainty regarding the timing and extent of Fed rate cuts also raised U.S. demand concerns.

Grain prices were all lower again last week. Favorable Brazil and Argentina weather forecasts and increased production forecasts drove corn and soybean prices lower through Thursday. Wheat prices, initially supported by rumors of increased Mexican and Chinese buying, moved lower through Thursday as well, pressured by otherwise weak export numbers and cheap Russian prices. Friday’s USDA WASDE release added to downward prices pressure with global ending stocks and world production coming in higher than expected for corn, soybeans and wheat. Wheat also suffered from increased Russian and Ukraine exports.

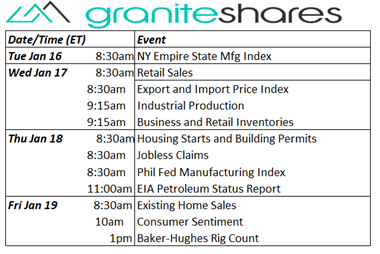

Coming Up This Week

Busy week with retail sales, housing starts, existing home sales and consumer sentiment headlining data releases.

Busy week with retail sales, housing starts, existing home sales and consumer sentiment headlining data releases.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.