Commodities & Precious Metals Weekly Report: Jan 28

Posted:

Key points

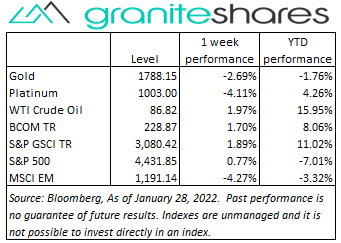

Energy prices moved higher with natural gas prices surging. WTI crude oil prices increased 2%, gasoline prices rose just under 4% and natural gas prices spiked, increasing 23%.

Energy prices moved higher with natural gas prices surging. WTI crude oil prices increased 2%, gasoline prices rose just under 4% and natural gas prices spiked, increasing 23%. - Grain prices were all higher as well. Chicago and Kansas wheat prices increased 0.8% and 1.1%, respectively. Corn prices increased 3.2% and soybean prices rose 3.9%.

- Precious metal prices fell. April gold and March silver futures prices lost 2.6% and 8.3%, respectively. Platinum prices fell 4.1%.

- Base metal prices were mainly lower. Copper and nickel prices dropped 4.7% and 6.7%, respectively, and zinc prices fell 0.7%. Aluminum prices increased 1.5%.

- The Bloomberg Commodity Index increased 1.7% benefiting from soaring natural gas prices and rising oil and grain prices. The base and precious metals sectors detracted from the index performance.

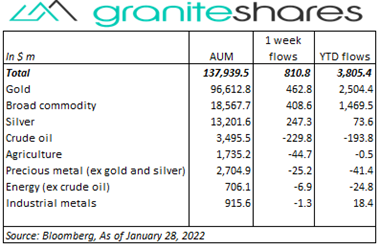

- Decent inflows ($811 million) into commodity ETPS primarily from gold ($463m) , broad commodity ($409m) and silver ($247m) ETPs inflows. Crude oil ETPs had the largest outflows (-$230m), followed by agricultural ETPs (-$45m).

Commentary

An extremely volatile week for U.S. stock markets with the Dow Jones Industrial Average swinging from down 1000 points (-3.3%) to close up 100 points (0.3%) on Monday. Uncertainty surrounding the 2-day FOMC meeting (beginning Tuesday and ending Wednesday) drove market performance as investors battled hawkish versus dovish outcomes. The FOMC announcement, leaving rates unchanged but strongly intimating rate hikes will begin in March followed by a possible balance sheet reduction soon afterwards, squelched a 2%-3% rally in all three major stock indexes and leaving them slightly lower to unchanged on the day. Tightening concerns, heightened by Thursday’s better-than-expected GDP release, moved markets lower Thursday only to see those concerns erased Friday with as-expected PCE Price and Employment Cost Index numbers lifting the three major indexes 2%-3% higher. The 10-year U.S. Treasury rate was also volatile, climbing 10bps through Thursday on aggressive-tightening concerns and then falling the remainder of the week to end almost unchanged. The U.S. dollar strengthened significantly last week, mainly as a result of Wednesday’s FOMC announcement. At week’s end, the S&P 500 Index increased 0.8% to 4,431.85, the Nasdaq Composite Index was practically unchanged at 13,770.6, the Dow Jones Industrial Average rose 1.3% to 34,726.20, the 10-year U.S. Treasury rate increased 1bp to 1.78% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) strengthened 1.7%.

An extremely volatile week for U.S. stock markets with the Dow Jones Industrial Average swinging from down 1000 points (-3.3%) to close up 100 points (0.3%) on Monday. Uncertainty surrounding the 2-day FOMC meeting (beginning Tuesday and ending Wednesday) drove market performance as investors battled hawkish versus dovish outcomes. The FOMC announcement, leaving rates unchanged but strongly intimating rate hikes will begin in March followed by a possible balance sheet reduction soon afterwards, squelched a 2%-3% rally in all three major stock indexes and leaving them slightly lower to unchanged on the day. Tightening concerns, heightened by Thursday’s better-than-expected GDP release, moved markets lower Thursday only to see those concerns erased Friday with as-expected PCE Price and Employment Cost Index numbers lifting the three major indexes 2%-3% higher. The 10-year U.S. Treasury rate was also volatile, climbing 10bps through Thursday on aggressive-tightening concerns and then falling the remainder of the week to end almost unchanged. The U.S. dollar strengthened significantly last week, mainly as a result of Wednesday’s FOMC announcement. At week’s end, the S&P 500 Index increased 0.8% to 4,431.85, the Nasdaq Composite Index was practically unchanged at 13,770.6, the Dow Jones Industrial Average rose 1.3% to 34,726.20, the 10-year U.S. Treasury rate increased 1bp to 1.78% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) strengthened 1.7%.

After falling a little over 2% Monday, oil prices resumed their climb higher supported by OPEC+ production difficulties, and geopolitical tensions in the Middle East and between Russia and Ukraine. Oil prices rose to finish the week flirting with 7-year highs, despite a sharply stronger U.S. dollar, a larger-than-expected increase in U.S. oil inventories and Fed-tightening concerns. Natural gas prices soared just shy of 23% last week, moving higher predominantly on cold weather in the U.S. Northeast and Midwest. The natural gas March futures contract increased 14.5% over Thursday and Friday.

The Russia-Ukraine situation and highly volatile equity markets prompted by uncertainty surrounding the FOMC announcement Wednesday pushed gold prices over 1% higher through Tuesday. Wednesday’s FOMC announcement and subsequent Jerome Powell press conference, confirming the Fed’s intent to move rates higher in March, contributed to a stronger U.S. dollar, moving gold prices 1.2% lower. Thursday’s better-than-expected GDP release, added to tightening expectations, moved the U.S. dollar higher and gold prices 2% lower. Silver prices moved sharply lower on the week, moving lower with gold and base metal prices.

Base metal prices moved lower last week, dropping as the U.S. Federal Reserve Bank prepares to increase rates in March. Investor expectations of slowing economic growth and, as a result, decreasing base metal demand as the Fed switches to a more restrictive monetary policy pushed copper and nickel prices lower. Aluminum prices were the exception, increasing with declining supplies due to high-energy-cost production cutbacks. Zinc prices, though down about ¾ percent on the week, also continued to be supported by smelter shutdowns due to high energy cost.

Grain prices were all higher again last week. Soybean and corn prices rose on lower South America production estimates and reports of large corn sales to China. Wheat prices continue to benefit from Russia-Ukraine tensions but finished well off their intraweek highs of up near 5% with increasing expectations the tensions may be resolved without conflict.

Coming up this week

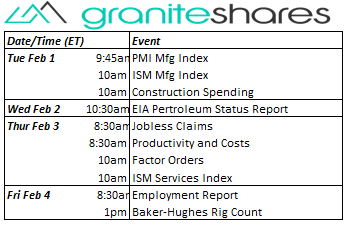

PMI and ISM indexes this week along with jobless claims with the week capped off with Friday’s employment report.

PMI and ISM indexes this week along with jobless claims with the week capped off with Friday’s employment report.- PMI and ISM Mfg Indexes and Construction Spending on Tuesday.

- Jobless Claims, Productivity and Costs, Factory Orders and ISM Services Index on Thursday.

- Employment Report on Friday.

- EIA Petroleum Status Report Wednesday and Baker-Hughes Rig Count on Friday.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.