Commodities & Precious Metals Weekly Report: Jul 28

Posted:

Key points

Energy prices, except for natural gas prices, all moved higher. WTI and Brent crude oil prices increased 4%, gasoline prices rose 5% and heating oil and gasoil prices gained 8%. Natural gas prices fell 3%.

Energy prices, except for natural gas prices, all moved higher. WTI and Brent crude oil prices increased 4%, gasoline prices rose 5% and heating oil and gasoil prices gained 8%. Natural gas prices fell 3%.- Wheat, corn and soybean prices fell 1%.

- Spot gold prices were practically unchanged while spot silver and platinum prices fell 1% and 2%, respectively.

- Nickel prices rose 7%, zinc prices gained 5% and copper prices increased 3%. Aluminum and lead prices rose 1%.

- The Bloomberg Commodity Index rose 1.1%. Most of the increase, again, was attributable to the energy sector with the base metals sector also contributing. All other sectors detracted from the Index performance.

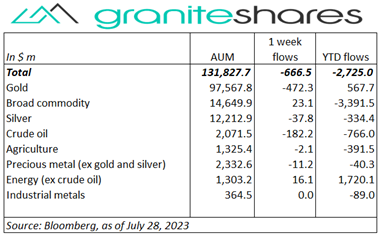

- Outflows last week, mainly from gold but also crude oil ETPs. Small inflows into broad commodity and energy (ex-crude oil) ETPs

Commentary

Stock markets moved higher last week, this time with the Nasdaq Composite Index outperforming both the Dow Jones Industrial Average and the S&P 500 Index. Markets moved higher through mid-week in expectation of the Fed’s tightening operations reaching their zenith after one last 25bp increase. Those expectations were seemingly met Wednesday after an as-expected 25bp hike in the fed funds target range and after somewhat supportive comments by Fed Chair Powell opining that the after effects of heretofore tightening possibly have yet to be seen. Those expectations changed Thursday, however, following smaller-than-expected initial jobless claims and greater-than-expected GDP growth, generating renewed concerns the Fed may find reason to tighten more (or keep rates higher longer), pushing all 3 indexes at least 1/2 percent lower and 10-year Treasury rates 13bps higher. Alas, Thursday’s concerns were lessened Friday with price and wage inflation data pointing to continued cooling. Both the headline and core PCE Price Index and the Employment Cost Index releases came in slightly better than expected, rejuvenating hopes of “peak rates” and a soon-to-be more benign Fed, powering stock markets markedly higher and partially reversing Thursday’s 10-year Treasury rate rise. For the week, the S&P 500 Index increased 1.0% to 4,582.23, the Nasdaq Composite Index rose 2.0% to 14,316.66, the Dow Jones Industrial Average gained 0.7% to close at 35,458.96, the 10-year U.S. Treasury rate increased 12bp to 3.96% and the U.S. dollar (as measured by the ICE U.S. Dollar index – DXY) strengthened 0.6%.

Stock markets moved higher last week, this time with the Nasdaq Composite Index outperforming both the Dow Jones Industrial Average and the S&P 500 Index. Markets moved higher through mid-week in expectation of the Fed’s tightening operations reaching their zenith after one last 25bp increase. Those expectations were seemingly met Wednesday after an as-expected 25bp hike in the fed funds target range and after somewhat supportive comments by Fed Chair Powell opining that the after effects of heretofore tightening possibly have yet to be seen. Those expectations changed Thursday, however, following smaller-than-expected initial jobless claims and greater-than-expected GDP growth, generating renewed concerns the Fed may find reason to tighten more (or keep rates higher longer), pushing all 3 indexes at least 1/2 percent lower and 10-year Treasury rates 13bps higher. Alas, Thursday’s concerns were lessened Friday with price and wage inflation data pointing to continued cooling. Both the headline and core PCE Price Index and the Employment Cost Index releases came in slightly better than expected, rejuvenating hopes of “peak rates” and a soon-to-be more benign Fed, powering stock markets markedly higher and partially reversing Thursday’s 10-year Treasury rate rise. For the week, the S&P 500 Index increased 1.0% to 4,582.23, the Nasdaq Composite Index rose 2.0% to 14,316.66, the Dow Jones Industrial Average gained 0.7% to close at 35,458.96, the 10-year U.S. Treasury rate increased 12bp to 3.96% and the U.S. dollar (as measured by the ICE U.S. Dollar index – DXY) strengthened 0.6%.

Oil prices moved higher last week, bolstered early in the week by Chinese pledges of economic stimulus and planned OPEC+ production cutbacks. Oil prices moved lower Wednesday, however, reacting to concerns the Fed may feel the need to continue to raise rates, smaller-than-expected drawdowns in oil and gasoline stocks and – as revealed Monday – on slowing business activity in the U.S. and Europe. Thursday’s smaller-than-expected initial jobless claims and greater-than-expected GDP growth diminished Fed demand-destruction concerns, moving prices higher. Friday’s better-than-expected inflation releases (i.e., the PCE Price Index and Employment Cost Index) buttressed soft-landing expectations, helping prices move higher as well.

A volatile week for gold prices with spot prices moving higher 0.6% through Wednesday, falling 1.4% Thursday and then gaining ¾ percent Friday to end the week almost unchanged. Increased hopes and expectations of a less aggressive Fed going forward before and following Wednesday’s FOMC decision were the primary impetus for the increase in gold prices through Wednesday. Smaller-than-expected initial jobless claims and greater-than-expected GDP growth renewed concerns of additional rate hikes (or rates remaining higher for longer), driving gold prices sharply lower. Those losses were partially recouped Friday after better-than-expected inflation data (i.e., PCE Price Index and ECI releases). Silver and platinum prices underperformed gold prices, falling 1% and 2%, respectively.

Base metal prices ended the week higher, overcoming concerns of lack of Chinese economic stimulus and ongoing central bank tightening. Prices moved higher early in the week, supported by Chinese pledges of economic stimulus. Uncertainty surrounding the Fed’s future monetary policy (following Fed Chair Powell’s comments Wednesday), Thursday’s better-than-expected U.S GDP and jobless claims numbers and no announcement of Chinese stimulus plans drove prices lower over Wednesday and Thursday. Prices, however, rebounded sharply Friday in the wake of lower-than-expected U.S. and European inflation data.

Wheat and corn prices moved sharply higher Monday following Russian attacks on Ukrainian grain storage facilities but moved lower the remainder of the week (both ending the week about 1% lower) in the absence of further attacks. Soybean prices moved in empathy to wheat and corn prices. Favorable longer-term weather forecasts also pressured prices lower as did falling soybean meal and soybean oil prices (with regards to soybean prices).

Coming Up This Week

PMI and ISM indexes Tuesday and Thursday with the main focuse Friday’s Employment Report.

PMI and ISM indexes Tuesday and Thursday with the main focuse Friday’s Employment Report.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.