Commodities & Precious Metals Weekly Report: Jun 11

Posted:

Key points

Energy prices were mainly higher last week. WTI and Brent crude oil prices increased 1.5% and 1%, respectively and gasoline and heating oil prices rose just over 2%. Natural gas prices increased almost 6.5%.

Energy prices were mainly higher last week. WTI and Brent crude oil prices increased 1.5% and 1%, respectively and gasoline and heating oil prices rose just over 2%. Natural gas prices increased almost 6.5%.- Grain prices were mixed both within categories of grain and with respect to front month and longer-dated contracts. Chicago wheat prices fell 1% while Kansas wheat prices gained ¼ percent. September Corn futures increased almost 4% while the front-month July contract only increased ¼ percent. The November soybean contract rose ¼ percent with the front month July contract falling almost 5%. December soybean oil contracts fell 1% much less than the front month contract which fell over 6%.

- Base metal prices were all higher with nickel and zinc prices performing the best. Nickel and zinc prices increased just over 1% and copper and aluminum prices increased about ¼ percent.

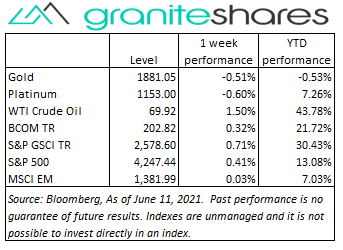

- Gold and platinum prices decreased last week while silver prices rose. Gold and platinum prices fell about ½ percent. Silver prices increased close to 1%.

- The Bloomberg Commodity Index increased 0.3%, supported by higher energy and base metal prices. The precious metals and grains sectors detracted from the Index’s performance.

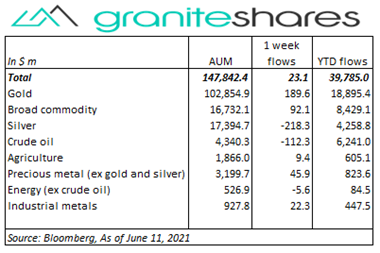

- Almost zero net inflows into commodity ETP last week resulting from small inflows into gold ($190mm) and broad commodity ($92mm) ETPs and small outflows from silver (-$220mm) and crude oil (-$110mm) ETPs.

Commentary

U.S stock markets moved lower prior to Thursday’s CPI release, reflecting the possibility the Fed may need to scale back its easy-money policies sooner than later. Despite CPI coming in above expectations, jumping 5% YoY and 0.6% MoM, stock prices generally moved higher with the S&P 500 Index hitting a record high and the Nasdaq Composite Index increasing 0.8%. Stock prices continued their move higher on Friday, though the Dow Jones Industrial Average ended the week lower while the S&P 500 and Nasdaq Composite Indexes moved higher. Interestingly, 10-year U.S. Treasury rates moved lower throughout the week, falling 8bps before the CPI release. For the week, the S&P 500 Index increased 0.4% to 4,247.44, the Nasdaq Composite Index increased 1.9% to 14,069.42, the Dow Jones Industrial Average fell 0.8% to 34,479.6, the 10-year U.S. Treasury rate fell 10bps to 1.46% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) strengthened ½ percent.

U.S stock markets moved lower prior to Thursday’s CPI release, reflecting the possibility the Fed may need to scale back its easy-money policies sooner than later. Despite CPI coming in above expectations, jumping 5% YoY and 0.6% MoM, stock prices generally moved higher with the S&P 500 Index hitting a record high and the Nasdaq Composite Index increasing 0.8%. Stock prices continued their move higher on Friday, though the Dow Jones Industrial Average ended the week lower while the S&P 500 and Nasdaq Composite Indexes moved higher. Interestingly, 10-year U.S. Treasury rates moved lower throughout the week, falling 8bps before the CPI release. For the week, the S&P 500 Index increased 0.4% to 4,247.44, the Nasdaq Composite Index increased 1.9% to 14,069.42, the Dow Jones Industrial Average fell 0.8% to 34,479.6, the 10-year U.S. Treasury rate fell 10bps to 1.46% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) strengthened ½ percent.

Oil prices moved higher again last week with WTI prices reaching levels not seen in over 2 years. Indications of strong demand (the IEA indicated OPEC+ would need to boost production to meet demand in the coming months) combined with OPEC+ production restraint and news sanctions on Iran would not be relaxed or removed any time soon, helped move oil prices higher. Wednesday’s EIA report showing a large, unexpected build in oil inventories and data released Monday showing Chinese imports had declined worked to cap gains.

Gold prices finished the week lower, hurt by a stronger U.S. dollar and risk-on investor sentiment. Thursday’s greater-than-expected CPI release initially did little to affect gold prices. Friday, however, saw gold prices drop close to 1% as market participants adopted the “transitory inflation” view with increasing expectations the Fed will maintain its current aggressively accommodative monetary policy, diminishing safe haven demand for gold.

Down nearly 1% through Thursday, copper prices rallied almost 1.2% Friday to finish the week slightly higher. Pressured by Chinese commitments to prevent “unreasonable” price moves, prices rose Friday with increasing “risk-on” investor sentiment following decreasing inflation concerns and declining expectations of central bank tightening.

Continued volatility in grain prices last week with a sharp rise in contango for soybean product contracts. For example, November soybean futures contracts increased 0.2% over the week while the July contract fell almost 5%. Thursday’s USDA WASDE report forecasting increased U.S. soybean stock pushed soybean prices lower Thrusday and Friday. Corn prices up over 5% through Thursday, partly as a result of a bullish WASDE report forecasting 8-year lows in U.S. corn supplies, fell almost 1% Friday as markets reassesed supply levels. Soybean oil futures moved sharply lower Friday on concerns President Biden may relax biofuel blending requirments.

Coming up this week

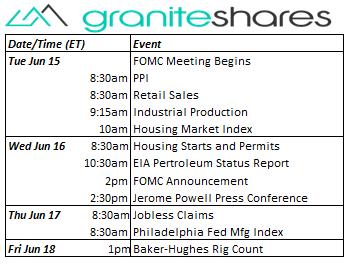

A busy data-week with PPI, Retail Sales and the 2-day FOMC meeting highlighting the week.

A busy data-week with PPI, Retail Sales and the 2-day FOMC meeting highlighting the week.- FOMC Meeting begins, PPI, Industrial Production and Housing Market Index on Tuesday.

- Housing Starts and Permits, FOMC Announcement and Jerome Powell Press Conference on Wednesday.

- Jobless Claims and Phil. Fed Mfg Index on Thursday.

- Consumer Sentiment on Friday.

- EIA petroleum status report on Wednesday and Baker-Hughes rig count on Friday.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.