Commodities & Precious Metals Weekly Report: Nov 19

Posted:

Key points

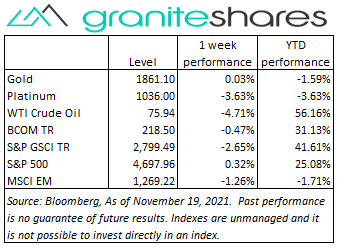

Energy prices, except for natural gas prices, were all lower last week. WTI crude oil prices declined just under 5%, Brent crude oil prices fell 3.5%, gasoline prices dropped 5% and heating oil prices fell 4.5%. Natural gas prices increased 5.5%.

Energy prices, except for natural gas prices, were all lower last week. WTI crude oil prices declined just under 5%, Brent crude oil prices fell 3.5%, gasoline prices dropped 5% and heating oil prices fell 4.5%. Natural gas prices increased 5.5%.- Grain prices were mixed. Wheat prices rose between 1/3 and ¾ percent and soybean prices gained 1.5%. Corn prices fell 1.5%.

- Precious metal prices finished the week lower. February gold futures prices fell almost 1% and silver prices dropped 2%. Platinum prices decreased slightly over 3.5%.

- Base metal prices were all lower except for nickel prices. Aluminum and zinc prices decreased almost 0.6% and copper prices fell 1.1%. Nickel prices were up 0.4%.

- The Bloomberg Commodity Index decreased ½ percent. Negative energy, base and precious metals sector performance was partially offset by positive performance in the agriculture sector.

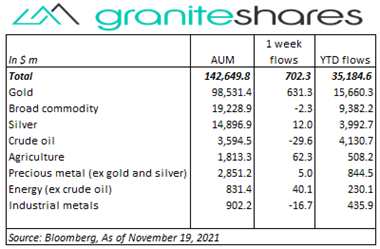

- Decent inflows into commodity ETPs ($702m) driven primarily by inflows into gold ETPs ($631m) and to a lesser extent by agriculture ($62m) and energy (ex-crude oil) ($40m) ETP inflows. Only small ETP outflows last week.

Commentary

Divergence in the major stock indexes last week with the S&P 500 and Nasdaq Composite Indexes increasing and the Dow Jones Industrial Average falling. A better-than-expected retail sales release and strong earnings reports moved markets higher through Tuesday though re-emerging fears of inflation and a more aggressive Fed pressured markets lower on Wednesday. The 10-year U.S. Treasury rate behaved oppositely, increasing 7bps through Tuesday and then falling almost 6bps Wednesday with increasing expectations of a more aggressive Fed precipitating slower economic growth. Rising Covid cases in Europe and Austria’s lockdown announcement increased concerns of slowing global economic growth and raised the possibility of rising Covid cases in the U.S. These concerns pushed the Nasdaq Composite Index higher (stay-at-home stocks benefiting), the Dow Jones Industrial Average lower (lockdown-free stocks hurt) and strengthened the U.S. dollar (because of its appeal as a safe-haven investment and because of likely continued easy-money policies in Europe in the face of renewed lockdowns). At week’s end, the S&P 500 Index increased 0.3% to 4,697.96, the Nasdaq Composite Index rose 1.2% to 16,057.40, the Dow Jones Industrial Average fell 1.4% to 35,602.18, the 10-year U.S. Treasury rate decreased 2bps to 1.55% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) strengthened 0.9%.

Divergence in the major stock indexes last week with the S&P 500 and Nasdaq Composite Indexes increasing and the Dow Jones Industrial Average falling. A better-than-expected retail sales release and strong earnings reports moved markets higher through Tuesday though re-emerging fears of inflation and a more aggressive Fed pressured markets lower on Wednesday. The 10-year U.S. Treasury rate behaved oppositely, increasing 7bps through Tuesday and then falling almost 6bps Wednesday with increasing expectations of a more aggressive Fed precipitating slower economic growth. Rising Covid cases in Europe and Austria’s lockdown announcement increased concerns of slowing global economic growth and raised the possibility of rising Covid cases in the U.S. These concerns pushed the Nasdaq Composite Index higher (stay-at-home stocks benefiting), the Dow Jones Industrial Average lower (lockdown-free stocks hurt) and strengthened the U.S. dollar (because of its appeal as a safe-haven investment and because of likely continued easy-money policies in Europe in the face of renewed lockdowns). At week’s end, the S&P 500 Index increased 0.3% to 4,697.96, the Nasdaq Composite Index rose 1.2% to 16,057.40, the Dow Jones Industrial Average fell 1.4% to 35,602.18, the 10-year U.S. Treasury rate decreased 2bps to 1.55% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) strengthened 0.9%.

Oil prices moved lower last week pressured by a myriad of factors. Increased shale oil production, prospects of coordinated strategic oil reserve releases and Europe’s surging Covid cases (and Austria’s lockdown) all combined to push oil prices lower. Wednesday’s EIA report showing falling oil and gasoline reserves did little to support prices and only resistance from South Korea and Japan to release reserves on Thursday supported oil prices. January natural gas futures prices moved almost 5.5% higher last week, pushed higher by strong LNG exports, Germany’s suspension of the Nord Stream 2 gas pipeline construction permit and forecasts of cold weather in Europe and the U.S.

Gold prices settled lower last week with increasing 10-year U.S. real rates and a stronger U.S. dollar pressuring prices lower. Europe’s (and China’s) surging Covid cases fortified expectations the ECB would continue its easy-money policies strengthening the U.S. dollar and pressuring gold prices lower. Nonetheless, 10-year U.S. real rates remain at historically low levels (-1.12%), perhaps reflecting the Fed’s reluctance or inability to more aggressively tighten monetary policy.

Copper prices moved almost 4% lower through Wednesday last week, pressured by rising LME inventories, slowing growth in the Chinese property sector, surging Europe and China Covid cases and a stronger U.S. dollar. Prices then rallied almost 3% the remainder of the week, buoyed most likely by short covering and, to some extent, by tighter China inventories due to Chinese VAT issues.

Soybean and wheat prices moved higher last week buoyed by strong export demand. Wheat prices continue to be supported by tight global supplies exacerbated by Russia’s wheat export tax. Corn prices ended the weak lower, hurt by falling oil prices affecting ethanol demand and prices.

Coming up this week

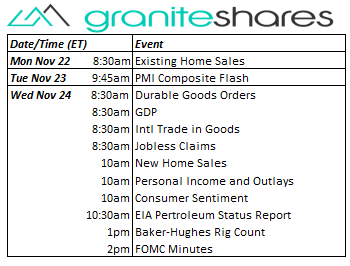

Busy holiday-shortened data week with most data releases jammed into Wednesday.

Busy holiday-shortened data week with most data releases jammed into Wednesday.- Existing Home Sales on Monday.

- PMI Composite Flash on Tuesday.

- Durable Goods Orders, GDP, Intl Trade in Goods, Jobless Claims, New Home Sales, Personal Income and Outlays and Consumer Sentiment on Wednesday.

- EIA Petroleum Status Report and Baker-Hughes Rig Count on Wednesday.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.