Commodities & Precious Metals Weekly Report: Nov 24

Posted:

Key points

Energy prices were mixed last week. WTI crude oil and gasoline prices were down about 1%, natural gas prices fell 4% and Brent crude oil prices were unchanged. Gasoil prices were up 3% and heating oil prices increased 2%.

Energy prices were mixed last week. WTI crude oil and gasoline prices were down about 1%, natural gas prices fell 4% and Brent crude oil prices were unchanged. Gasoil prices were up 3% and heating oil prices increased 2%.- Grain prices were mostly lower with Chicago wheat prices bucking the trend and rising less than ½ percent. Kansas City wheat prices fell 3% and corn and soybean prices dropped 1%.

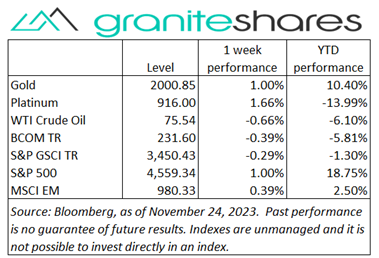

- Spot gold prices rose 1%, spot silver prices increased 3% and platinum prices gained 4%.

- Zinc and aluminum prices fell under 1% and nickel prices lost 2%. Copper prices rose 4% and lead prices increased 5%.

- The Bloomberg Commodity Index fell 0.4%. Losses in the energy, grains and livestock sectors were partially offset by gains in the precious metals sector.

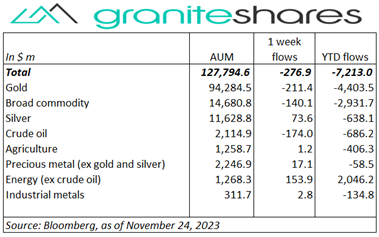

- Outflows last week, all from gold, broad commodity and crude oil ETPs. Decent sized offsetting inflows into energy (ex-crude oil) ETPs reduced net outflows.

Commentary

Major stock market indexes moved higher yet again last week. Stable longer-term Treasury rates (at levels significantly below 5%) and more weak economic data (falling home sales, PMI job cuts) provided the major impetus for the move higher, bolstering expectations of sooner-than-previously expected rate cuts. Interestingly, the Nasdaq Composite Index fared the worst last week, affected more by earnings concerns (after Nvidia delayed chip design and production for the Chinese market) than rate outlooks. The Dow Jones Industrial Average performed the best last week despite concerns surrounding consumer spending, perhaps buoyed by less tech-stock exposure. For the week, the S&P 500 Index rose 1.0% to 4,559.34, the Nasdaq Composite Index increased 0.9% to 14,250.09 the Dow Jones Industrial Average gained 1.3% to 35,390.57, the 10-year U.S. Treasury rate increased 3bps to 4.47% and the U.S. dollar (as measured by the ICE U.S. Dollar index – DXY) weakened 0.5%.

Major stock market indexes moved higher yet again last week. Stable longer-term Treasury rates (at levels significantly below 5%) and more weak economic data (falling home sales, PMI job cuts) provided the major impetus for the move higher, bolstering expectations of sooner-than-previously expected rate cuts. Interestingly, the Nasdaq Composite Index fared the worst last week, affected more by earnings concerns (after Nvidia delayed chip design and production for the Chinese market) than rate outlooks. The Dow Jones Industrial Average performed the best last week despite concerns surrounding consumer spending, perhaps buoyed by less tech-stock exposure. For the week, the S&P 500 Index rose 1.0% to 4,559.34, the Nasdaq Composite Index increased 0.9% to 14,250.09 the Dow Jones Industrial Average gained 1.3% to 35,390.57, the 10-year U.S. Treasury rate increased 3bps to 4.47% and the U.S. dollar (as measured by the ICE U.S. Dollar index – DXY) weakened 0.5%.

Oil prices ended slightly lower on the week, belying volatility due to OPEC+ supply concerns. Prices rose north of 2% Monday, climbing on OPEC+ comments that they were considering additional cutbacks. Prices then moved sharply lower Wednesday and Friday following a postponement of the scheduled November 26 OPEC+ meeting (due to internal cutback/production disagreements) and a larger-than-expected build in U.S. inventories.

Spot gold prices rose again last week, propped up by dovish FOMC minutes and increasing expectations of sooner-than-previously-expected rate cuts. Stable longer-term Treasury rates (well below 5%), a continued slide lower in the U.S. dollar and weakish economic data added to peak rate expectations, moving gold, silver and platinum prices higher on the week.

Copper prices moved higher as well last week, benefiting from additional Chinese stimulus, a stronger yuan/weaker dollar and mining supply disruptions. The major impetus for higher prices belongs to the PBoC’s intent to support distressed property developers.

Grain prices generally moved lower. Slightly improved Argentina and Brazil weather forecasts seemed to be the major reason prices moved lower followed by lackluster soybean, corn and export demand.

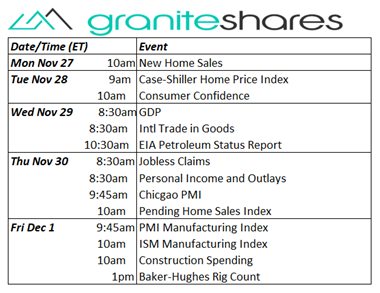

Coming Up This Week

GDP, PCE Price Index and PMI and ISM Mfg Indexes of importance this week.

GDP, PCE Price Index and PMI and ISM Mfg Indexes of importance this week.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.