Commodities & Precious Metals Weekly Report: Oct 14

Posted:

Key points

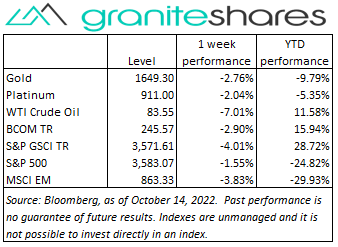

Energy prices were all lower last week. WTI and Brent crude oil prices decreased 7% and 6%, respectively. Heating oil, gasoil and gasoline prices fell between 5% and 6%. Natural gas prices lost 2%.

Energy prices were all lower last week. WTI and Brent crude oil prices decreased 7% and 6%, respectively. Heating oil, gasoil and gasoline prices fell between 5% and 6%. Natural gas prices lost 2%.- Grain prices were mixed. Wheat prices were down 2%. Corn and soybean prices increased 1%.

- Precious metal prices were all lower. Spot gold prices fell 3%. Spot silver prices dropped 9% and spot platinum prices decreased 1%.

- Base metal prices were mixed. Nickel and zinc prices fell between 2% and 3%. Aluminum prices were practically unchanged and copper prices increased 1%.

- The Bloomberg Commodity Index decreased 2.9%, mainly as result of falling energy and precious metal prices.

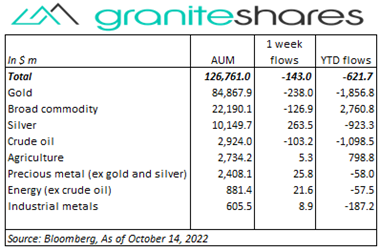

- Small ETP outflows last week. Gold (-$238m), broad commodity (-$127m) and crude oil (-$103m) ETP outflows were primarily offset by silver ($264m) ETP inflows.

Commentary

A volatile week with all 3 major stock indexes moving lower through Wednesday and then swinging wildly Thursday and Friday both intra- and interday. Prices moved lower early in the week as investors braced for PPI and FOMC minutes Wednesday and CPI Thursday. Russia-Ukraine war flare ups and Biden administration bans on China semi-conductor exports added to market malaise. Wednesday’s worse-than-expected PPI release and FOMC minutes expressing concerns over persistent, high levels of inflation while lamenting a strong job market seemingly had little effect on markets. Thursday’s CPI release showing core CPI increasing at a YoY rate not seen in 40 years, initially pushed stock prices sharply lower with the Dow Jones Industrial Average, for example, falling 500 points. Prices, however, then drastically reversed with all 3 major indexes ending the day north of 2% higher, perhaps buoyed by the fact CPI, while higher, had moved lower versus the two prior months or perhaps in expectations of good earnings reports to be released Friday. That sentiment or expectations, if they indeed existed, changed Friday with all 3 major stock market indexes, initially strongly continuing Thursday’s move higher, suddenly U-turned to end the day markedly lower. The move lower came despite better-than-expected earnings reports from JPM Chase, Citi and Wells Fargo. The Nasdaq Composite Index, the worst performer for the week, was also the worst performer Friday, falling 3.1%. The 10-year Treasury rate moved 14bps higher last week with real rates falling 6bps to 1.55% and 10-year inflation expectations increasing 20bps to 2.47%. At week’s end, the S&P 500 Index decreased 1.6% to close at 3,583.07, the Nasdaq Composite Index dropped 3.1% to 10,321.39, the Dow Jones Industrial Average rose 1.2% to 29,634.83, the 10-year U.S. Treasury rate rose 14bps to 4.03% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) strengthened 0.4%.

A volatile week with all 3 major stock indexes moving lower through Wednesday and then swinging wildly Thursday and Friday both intra- and interday. Prices moved lower early in the week as investors braced for PPI and FOMC minutes Wednesday and CPI Thursday. Russia-Ukraine war flare ups and Biden administration bans on China semi-conductor exports added to market malaise. Wednesday’s worse-than-expected PPI release and FOMC minutes expressing concerns over persistent, high levels of inflation while lamenting a strong job market seemingly had little effect on markets. Thursday’s CPI release showing core CPI increasing at a YoY rate not seen in 40 years, initially pushed stock prices sharply lower with the Dow Jones Industrial Average, for example, falling 500 points. Prices, however, then drastically reversed with all 3 major indexes ending the day north of 2% higher, perhaps buoyed by the fact CPI, while higher, had moved lower versus the two prior months or perhaps in expectations of good earnings reports to be released Friday. That sentiment or expectations, if they indeed existed, changed Friday with all 3 major stock market indexes, initially strongly continuing Thursday’s move higher, suddenly U-turned to end the day markedly lower. The move lower came despite better-than-expected earnings reports from JPM Chase, Citi and Wells Fargo. The Nasdaq Composite Index, the worst performer for the week, was also the worst performer Friday, falling 3.1%. The 10-year Treasury rate moved 14bps higher last week with real rates falling 6bps to 1.55% and 10-year inflation expectations increasing 20bps to 2.47%. At week’s end, the S&P 500 Index decreased 1.6% to close at 3,583.07, the Nasdaq Composite Index dropped 3.1% to 10,321.39, the Dow Jones Industrial Average rose 1.2% to 29,634.83, the 10-year U.S. Treasury rate rose 14bps to 4.03% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) strengthened 0.4%.

Except for Thursday, oil prices declined every single day last week. Growing expectations of central-bank induced recessions – exacerbated by Thursday’s worse-than-expected U.S. CPI release – combined with increased Covid cases in China pushed WTI crude oil prices 7% lower on the week. Thursday’s uptick in prices occurred as the EIA reported a much larger-than-expected drop in distillate inventories just before the onset of increased winter heating oil demand. A stronger U.S. dollar also contributed to lower prices.

Precious metal prices were all lower last with silver prices finishing the week markedly lower. A stronger U.S. dollar, buoyed by expectations of continued aggressive tightening by the U.S. Federal Reserve Bank, was the main driving force behind weakness in precious metal prices. Thursday’s worse-than-expected CPI release resulted in a muted response by gold prices with the U.S. dollar actually weakening that day and stock markets rallying sharply. Prices fell sharply Friday, however, with both stock markets and the U.S. dollar reversing direction. Spot silver prices significantly underperformed spot gold prices last week, falling just over 9%.

Base metal prices were mixed last week. Copper prices ended the week higher on supply concerns spurred by a sharp increase in LME canceled warrants and a 10% decline in Chilean copper production in August. Aluminum prices moved lower on rising inventories offsetting fears of a ban on Russian imports. Global recession concerns (particularly in China as a result of their continued zero-tolerance Covid policies) and a stronger U.S. dollarr either capped gains or pressured base metal prices lower as well.

Wheat prices ended the week about 2% lower despite Monday’s 6% price surge. Russia-Ukraine war escalations over the previous weekend had increased fears of continued, sharp reprisals from Russia including the blocking of wheat shipping lanes. Those fears diminished over the week while global recession fear increased. Soybean prices gained about 1% last week benefiting primarily from strong export demand and an unexpected reduction in harvest yield in Wednesday’s USDA Crop Production Report. Corn prices rose on no new news.

Coming up this week

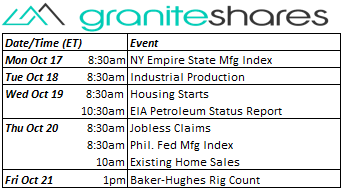

Sparse data week including housing starts and home sales data, industrial production and NY Empire State and Phil. Fed Mfg Indexes.

Sparse data week including housing starts and home sales data, industrial production and NY Empire State and Phil. Fed Mfg Indexes.- NY Empire State Mfg Index on Monday.

- Industrial Production on Tuesday.

- Housing Starts on Wednesday.

- Jobless Claims, Phil. Fed Mfg Index and Existing Home Sales on Thursday.

- EIA Petroleum Status Report Thursday and Baker-Hughes Rig Count on Friday.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.