Commodities & Precious Metals Weekly Report: Sep 3

Posted:

Key points

Energy prices moved higher again last week with natural gas prices increasing the most. Natural gas prices increased almost 7.5%. WTI and Brent crude oil prices increased 0.8% and 1.3%, respectively and gasoline prices rose 2%.

Energy prices moved higher again last week with natural gas prices increasing the most. Natural gas prices increased almost 7.5%. WTI and Brent crude oil prices increased 0.8% and 1.3%, respectively and gasoline prices rose 2%.- Grain prices all fell last week. Chicago and Kansas wheat lost 0.1% and 0.9%, respectively, while corn prices fell 5.3%. Soybean prices decreased 2.5%.

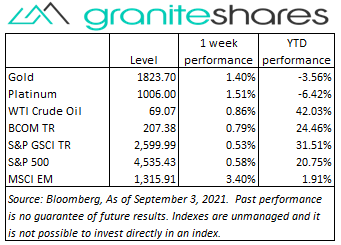

- Precious metal prices ended the week higher again, too. Gold prices increased 1.4%, silver prices rose 2.9% and platinum prices gained 1.5%.

- Base metal prices were mixed with aluminum and nickel prices recording decent gains and copper and zinc prices falling slightly or unchanged. Aluminum prices increased 3% and nickel prices rose 4%.

- The Bloomberg Commodity Index moved higher again last week, increasing 0.8%. The energy, base and precious metals sectors contributed to performance while the agriculture sector detracted.

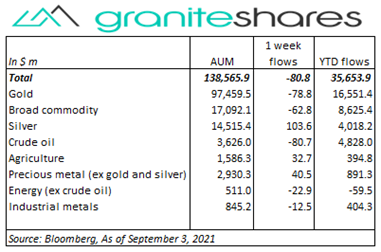

- Small net ETP outflows last week. Gold (-$80m), crude oil (-$80m) and broad commodity (-$63m) ETP outflows were mostly offset by silver ($110m), agriculture ($33m) and precious metals (ex-gold and silver) ($40m) ETP inflows.

Commentary

U.S. stock markets were mainly higher last week with the Nasdaq Composite Index and the S&P 500 Index closing at or just below record highs but with the Dow Jones Industrial Average finishing lower on the week. Growth stocks performed better than value stocks, buoyed by disappointing payroll reports and flagging consumer confidence – both attributed to Delta variant-related concerns and restrictions. Wednesday’s much weaker-than-expected ADP payroll report was substantiated by Friday’s much weaker-than-expected U.S. non-farm payroll report with markets overall reacting to the “bad news” as “good news” believing weak economic data would forestall the Fed from tightening monetary policy anytime soon. The 10-year U.S. Treasury reacted oppositely, increasing 4bps after the release of U.S. non-farm payroll report perhaps reflecting inflation concerns given the likelihood of the Fed to continue with its ultra-accommodative monetary policy and the U.S. dollar weakened, seemingly reflecting those same concerns. For the week, the S&P 500 Index increased 0.6% to 4,535.43, the Nasdaq Composite Index rose 1.6% to 15,363.50, the Dow Jones Industrial Average fell 0.2% to 35,369.35, the 10-year U.S. Treasury rate increased 2bps to 1.33% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) weakened 0.7% percent.

U.S. stock markets were mainly higher last week with the Nasdaq Composite Index and the S&P 500 Index closing at or just below record highs but with the Dow Jones Industrial Average finishing lower on the week. Growth stocks performed better than value stocks, buoyed by disappointing payroll reports and flagging consumer confidence – both attributed to Delta variant-related concerns and restrictions. Wednesday’s much weaker-than-expected ADP payroll report was substantiated by Friday’s much weaker-than-expected U.S. non-farm payroll report with markets overall reacting to the “bad news” as “good news” believing weak economic data would forestall the Fed from tightening monetary policy anytime soon. The 10-year U.S. Treasury reacted oppositely, increasing 4bps after the release of U.S. non-farm payroll report perhaps reflecting inflation concerns given the likelihood of the Fed to continue with its ultra-accommodative monetary policy and the U.S. dollar weakened, seemingly reflecting those same concerns. For the week, the S&P 500 Index increased 0.6% to 4,535.43, the Nasdaq Composite Index rose 1.6% to 15,363.50, the Dow Jones Industrial Average fell 0.2% to 35,369.35, the 10-year U.S. Treasury rate increased 2bps to 1.33% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) weakened 0.7% percent.

Oil prices moved higher last week supported by production shutdowns due to Hurricane Ida and renewed optimism of increased demand next year. Wednesday’s EIA report showed a much steeper-than-expected drop in oil inventories but also showed a greater-than-expected climb in gasoline stocks. The climb in gasoline inventories was attributed to reduced driving in the Northeast due to Tropical Storm Henri. Friday’s much weaker-than-expected U.S. payroll report sent WTI crude prices almost 1% lower cutting weekly gains by more than half.

Consolidating from the previous week’s move higher (due to Fed Chairman Powell’s comments cautioning against tightening monetary policy based on “a temporary fluctuation in inflation”), gold prices fell almost ½ percent through Thursday. Contrasting economic data, including a much weaker-than-expected ADP payroll report Wednesday and falling jobless claims released Thursday, limited gold price moves. Friday’s much weaker-than-expected U.S. payroll report, decreasing expectations of Fed tightening before year end, moved gold prices 1 ¼ percent higher.

Aluminum prices hit 10-year highs last week powered higher by Chinese production restrictions. China, which produces 60% of the world’s aluminum, has forced production cutbacks both because of power shortages and in an attempt to reduce pollution. Nickel prices also moved higher supported by strong stainless steel and EV-related demand. Slowing Chinese and European manufacturing activity along with China releasing metal reserves capped gains last week while a weaker U.S. dollar, primarily as a result of Friday’s much weaker-than-expected U.S. payroll report, supported prices.

Lessening weather concerns and Hurricane Ida-related export concerns helped push grain prices lower last week. Uncertainty surrounding the duration of the shutdown of the Port of Louisiana and its concomitant effect on grain exports contributed to weaker grain prices across the board. Grain prices rebounded Thursday and Friday from lows set Wednesday partly as a result of a weaker U.S. dollar and partly as a result of a relief rally after USDA export numbers showed no downside surprises.

Coming up this week

Very, very light holiday-shortened data week.

Very, very light holiday-shortened data week.- Jobless Claims on Thursday.

- PPI on Friday.

- EIA Petroleum Status Report on Thursday and Baker-Hughes Rig Count on Friday.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.