Outlook for Gold? A New Take on the Oldest Asset

Posted:

In a world of exotic assets and fast trading, what has become of the world’s oldest asset, gold? Modern finance, where the pursuit of endless sophistication is often confused with success itself, has forced investors to ask a pivotal question: is gold obsolete? Importantly, this question is not a matter of whether gold is overvalued, of growth stocks versus value stocks, or even which key rates to overweight in the bond portfolio. It is simply a question of whether gold has become too outmoded for the technologized portfolio.

The sobering answer, of course, is a resounding no. For all of our best efforts (including imaginary assets with non-imaginary values), we still have not come up with a better way to replace the diversification value, interest rate sensitivity and the stability that gold delivers in one accessible instrument.

Diversification

After the volatility pause of 2017, it became easy for investors to neglect the rationale for diversifying assets. After all, why add any assets with a correlation less than 1.000 when the market surges skyward? Such were the animal spirits that it was actually far more difficult to pick losers than winners; indeed amongst S&P 500 stocks, investors faced only a 1 in 25 chance of selecting a stock with a 25% or greater loss. The following year, however, Mr. Market gave investors a free (or not so free) audit in Markowitz 101 on the importance of diversification. The odds of a picking a stock with a 25% or greater loss increased five-fold from 4% to over 21%.

Learn More: 3 Reasons for Gold

The Q4 downturn in equities illustrated that this Nobel Prize-winning insight is as valid today as it was 67 years ago: correlations are the underpinnings of a portfolio. In this light, value of gold in a portfolio is not that it is a better investment, but merely a different investment; technology has not displaced this golden rule of diversification.

Interest Rates

When the Fed has shifted from continued hiking and contractions to pausing in a matter of months, with even expectations of outright easing, gold’s status as a hybrid commodity-currency brings value. Interest rates are a fundamental input to both commodities and currencies, influencing the carrying cost of the former and the relative yields of the latter.

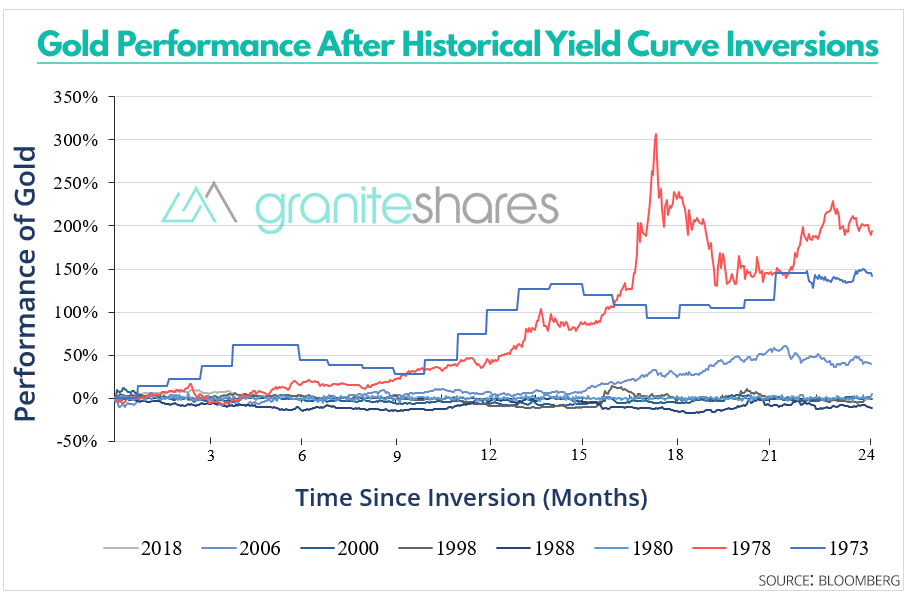

The role of gold, however, extends beyond playing accommodative shifts in monetary policy; gold more importantly can respond to the rapidity and volatility of change in Fed policy. This dynamic can be seen in the flattening and partial inversion of the yield curve, along with reduced expectations for global economic growth. While market theorists such as Yardeni will readily admit the yield curve-recession pattern is based on a sample size of seven, the ability of gold to respond to interest rate risk is meaningful.

Stability

If gold can afford diversification and interest rate hedging benefits, the question often posed is, Why is gold needed when investors could instead directly target these characteristics, eliminating gold as the middleman? For all of advances in program trading and derivative strategies, old-fashioned gold may still be the simplest and most intuitive means of accessing these desirable portfolio traits. The legitimate concerns raised over the manipulation of the VIX Index, and the collapse of many VIX-linked funds, illustrate that these strategies may not be suitable, or stable enough, for all investors.

Related: You May Know Gold, But Do You Know Platinum?

This feature lends a new meaning to the convenience yield of gold, a value that is difficult to discount. This is not to say that gold does not exhibit volatility; such a statement is as naïve as saying gold does not feature its own, organic return. The key point is that the age, history and, quite frankly, lack of novelty of gold, far from being detractors, are the cornerstones of its utility in a modern portfolio. Far from being obsolete, gold may tackle complex problems with a simple, inexpensive solution.