Commodities & Precious Metals Weekly Report: Jan 21

Posted:

Key points

Energy prices, except for natural gas prices, moved higher. Crude and heating oil prices increased around 2% and gasoline prices rose 1%. Natural gas prices fell over 7%.

Energy prices, except for natural gas prices, moved higher. Crude and heating oil prices increased around 2% and gasoline prices rose 1%. Natural gas prices fell over 7%.- Grain prices were all higher as well. Chicago and Kansas wheat prices jumped 5.2% and 6.5%, respectively. Corn and soybean prices rose 3.3%.

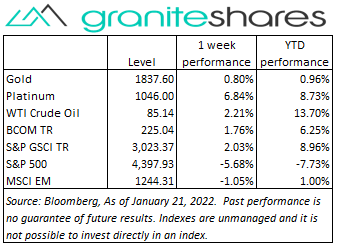

- Precious metal prices also moved higher. April gold and March silver futures prices increased 0.8% and 6.1%, respectively. Platinum prices gained 6.8%.

- Base metal prices moved higher, too. Nickel and zinc prices increased 8.5% and 3.5%, respectively, copper prices rose 2.3% and aluminum prices gained 2.1%.

- The Bloomberg Commodity Index rose again, increasing 1.8% primarily benefiting from increasing grains and precious and base metals prices. The energy sector was the only negative performing sector due to sharply declining natural gas prices.

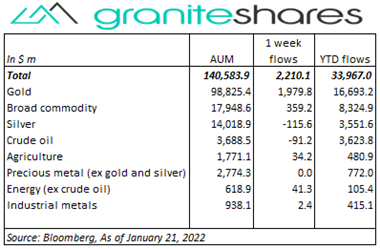

- Large inflows ($2.2 billion) into commodity ETPS with gold ETP inflows leading the way. Gold ETPs saw inflows of just under $2 billion followed by broad commodity ETPs with inflows of $359 million. crude oil and silver ETPs had combined outflows of just over $200 million.

Commentary

Another volatile week for U.S. stock markets with all 3 major indexes dropping 1% or more each day of the holiday-shortened week. Investor nervousness surrounding tightening Fed monetary policy was the main driving force behind last week’s move lower, with growing concerns of higher U.S interest rates decreasing valuations of most stocks but especially of growth/tech stocks. Year-to-date, the S&P 500 Index is down 7.7%, the Nasdaq Composite Index is lower by 12.0% and the Dow Jones Industrial Average is down 5.7%. Despite some notable exceptions (including Netflix and Peloton), earnings reports YTD have been predominantly positive (ie, beating expectations) helping to partially alleviate concerns of falling profit margins due to rising input costs. Thursday’s larger-than-expected jobless claims and Friday’s weaker-than-expected retail sales and existing home sales releases helped move 10-year U.S. Treasury lower but did nothing to reduce stock valuation concerns due to fears of rising rates. The 10-year U.S. Treasury rate, up over 8bps through Wednesday, actually ended the week lower with falling inflation expectations (-11bps) offsetting rising real rates (+9bps). At week’s end, the S&P 500 Index decreased 5.7% to 4,397.93, the Nasdaq Composite Index dropped 7.5% to 13,768.9, the Dow Jones Industrial Average fell 4.6% to 34,265.5, the 10-year U.S. Treasury rate decreased 2bps to 1.77% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) strengthened 0.5%.

Another volatile week for U.S. stock markets with all 3 major indexes dropping 1% or more each day of the holiday-shortened week. Investor nervousness surrounding tightening Fed monetary policy was the main driving force behind last week’s move lower, with growing concerns of higher U.S interest rates decreasing valuations of most stocks but especially of growth/tech stocks. Year-to-date, the S&P 500 Index is down 7.7%, the Nasdaq Composite Index is lower by 12.0% and the Dow Jones Industrial Average is down 5.7%. Despite some notable exceptions (including Netflix and Peloton), earnings reports YTD have been predominantly positive (ie, beating expectations) helping to partially alleviate concerns of falling profit margins due to rising input costs. Thursday’s larger-than-expected jobless claims and Friday’s weaker-than-expected retail sales and existing home sales releases helped move 10-year U.S. Treasury lower but did nothing to reduce stock valuation concerns due to fears of rising rates. The 10-year U.S. Treasury rate, up over 8bps through Wednesday, actually ended the week lower with falling inflation expectations (-11bps) offsetting rising real rates (+9bps). At week’s end, the S&P 500 Index decreased 5.7% to 4,397.93, the Nasdaq Composite Index dropped 7.5% to 13,768.9, the Dow Jones Industrial Average fell 4.6% to 34,265.5, the 10-year U.S. Treasury rate decreased 2bps to 1.77% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) strengthened 0.5%.

Middle East (Houthi attacks on UAE oil facilities) and Russia-Ukraine-US political tensions along with persistent OPEC+ production shortfalls helped push WTI crude oil prices to 7-year highs mid-week. WTI crude oil prices moved off Wednesday’s high following Thursday’s EIA report showing a build in U.S. oil inventories and a large increase in gasoline stocks though oil prices still finished 2% higher on the week.

Gold prices moved higher last week, buoyed by geo-political concerns surrounding Ukraine and Russia, Houthi attacks on UAE oil facilities and sharply falling U.S. stock markets. Up 1.5% through Wednesday, gold prices fell almost 0.6% Friday on no real news but perhaps as a result of declining 10-year U.S. interest rates and profit taking before the weekend and this week’s Fed meeting. Silver prices increased more than gold prices benefiting from higher base metal prices. Platinum prices moved higher with gold prices but also benefited from soaring palladium prices.

Nickel prices moved higher again last week, climbing 8.5% on the back of continued strong stainless steel and EV-battery demand and falling inventory levels. Copper prices moved higher as well supported by PBoC stimulus and strong demand. Copper prices, up 3.7% through Thursday, fell 1.3% Friday on weaker-than-expected Chinese economic numbers, a stronger U.S. dollar and falling U.S. stock markets.

Grain prices were all higher last week with wheat prices leading the way. Increased Ukraine-Russia concerns helped move wheat and corn prices higher with building fears of Ukraine export disruption (Ukraine is the 4th largest exporter of wheat and corn). Weather concerns in Argentina and Brazil have somewhat dissipated, working to cap corn and soybean price gains.

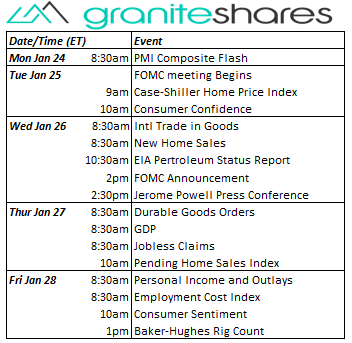

Coming up this week

Busy data-week with a 2-day FOMC meeting, GDP, home sales data and inflation data.

Busy data-week with a 2-day FOMC meeting, GDP, home sales data and inflation data.- PMI Composite Flash on Monday.

- FOMC Meeting Begins, Case-Shiller Home Price Index and Consumer Confidence on Tuesday.

- Intl Trade in Goods, New Home Sale, FOMC Announcement and Jerome Powell Press Conference on Wednesday.

- Durable Goods Orders, GDP, Jobless Claims, and Pending Homes Sales Index on Thursday.

- Personal Income and Outlays, Employment Cost Index and Consumer Sentiment on Friday.

- EIA Petroleum Status Report Wednesday and Baker-Hughes Rig Count on Friday.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.