Commodities & Precious Metals Weekly Report: Oct 8

Posted:

Key points

Energy prices, except for natural gas prices, moved higher again last week. WTI and Brent crude oil prices increased between 4% and 4.5%, gasoline prices rose over 5% and gasoil prices increased 6.5%. Natural gas prices fell 1%.

Energy prices, except for natural gas prices, moved higher again last week. WTI and Brent crude oil prices increased between 4% and 4.5%, gasoline prices rose over 5% and gasoil prices increased 6.5%. Natural gas prices fell 1%.- Grain prices were lower as well with wheat prices falling the most. Chicago and Kansas wheat prices fell 3%, corn prices lost 2% and soybean prices edged lower, losing 0.3%. Soybean oil prices increased 6.5%.

- Cotton prices continued their move higher, increasing almost 6%.

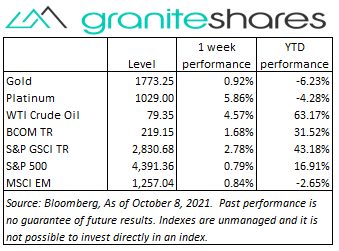

- Precious metal prices were mostly higher. Gold December futures prices were unchanged while silver prices increased 3/4 percent. Platinum prices surged, gaining almost 6%.

- Base metal prices moved higher last week with nickel prices gaining the most. Nickel and zinc prices rose 7.0% and 5.8%, respectively. Aluminum and copper prices increased 3.8% and 2.0%, respectively.

- The Bloomberg Commodity Index increased 1.7%, moving higher primarily on the back of positive energy and base metal performance. Only the grains sector detracted from last week’s performance.

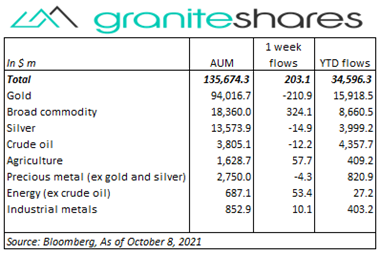

- $200 million net inflows into ETPs last week, mainly from inflows into broad commodity ETPs. Broad commodity ($324m), agriculture ($58m) and energy (ex-crude oil) ($53m) ETP inflows were partially offset by gold (-$211m) ETP outflows.

Commentary

A bumpy start last week with major U.S. stock indexes falling sharply and with the Nasdaq Composite Index faring the worst by far. Increasing inflation and Fed-tapering concerns, spurred by Friday’s PCE price index release, combined with a debt-ceiling overhang, pushed 10-year U.S. Treasury rates higher and stock prices – especially tech stock prices – lower (Facebook’s unprecedented outage Monday also affected the tech-heavy Nasdaq Composite Index). Stock markets rebounded sharply Tuesday and then continued higher through Thursday buoyed by a better-than-expected ISM services index release, falling weekly and continued jobless claims and substantive progress on a short-term debt ceiling extension. Friday’s much weaker-than-expected payroll report moved stock markets slightly lower while at the same time pulling the 10-year U.S. Treasury rate above 1.6%. For the week, the S&P 500 Index rose 0.8% to 4,392.36, the Nasdaq Composite Index increased 0.1% to 14,579.50, the Dow Jones Industrial Average gained 1.2% to 34,746.71, the 10-year U.S. Treasury rate jumped 15bp to 1.61% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) was practically unchanged.

A bumpy start last week with major U.S. stock indexes falling sharply and with the Nasdaq Composite Index faring the worst by far. Increasing inflation and Fed-tapering concerns, spurred by Friday’s PCE price index release, combined with a debt-ceiling overhang, pushed 10-year U.S. Treasury rates higher and stock prices – especially tech stock prices – lower (Facebook’s unprecedented outage Monday also affected the tech-heavy Nasdaq Composite Index). Stock markets rebounded sharply Tuesday and then continued higher through Thursday buoyed by a better-than-expected ISM services index release, falling weekly and continued jobless claims and substantive progress on a short-term debt ceiling extension. Friday’s much weaker-than-expected payroll report moved stock markets slightly lower while at the same time pulling the 10-year U.S. Treasury rate above 1.6%. For the week, the S&P 500 Index rose 0.8% to 4,392.36, the Nasdaq Composite Index increased 0.1% to 14,579.50, the Dow Jones Industrial Average gained 1.2% to 34,746.71, the 10-year U.S. Treasury rate jumped 15bp to 1.61% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) was practically unchanged.

Oil prices moved higher again last week, propelled by strong demand and as OPEC+ maintained its planned, gradual production increases following Monday’s meeting. Oil prices paused briefly Wednesday following a greater-than-expected U.S. inventory build, the Biden administration considering releasing SPR reserves and a sharp drop in natural gas prices precipitated by Russian President Putin’s announcement he would work to increase natural gas production and exports. Oil prices resumed their path higher the remainder of the week with WTI crude oil prices reaching levels not seen in 7 years and with Brent crude oil prices closing above $81/barrel.

Gold December futures prices finished the week almost unchanged, moving higher Monday on the back of sharply declining equity prices only to move lower the remainder of the week. Central bank tightening angst, rising longer-term U.S. interest rates and strong economic reports pressured prices lower through Thursday. Friday’s much weaker-than-expected U.S. payroll report initially sent gold prices almost 1% higher as investors lowered expectations of imminent Fed tightening only to see those gains erased by the close of U.S. trading with renewed uncertainty regarding changes in U.S. Federal Reserve Bank monetary policy.

Base metal prices moved sharply higher last week predominately because of falling inventory levels despite reduced Chinese demand. Production concerns in Peru (the world’s second largest copper producer behind Chile) increased following the blockage of a major mining road as part of a protest against the government while Chilean production remains hindered by strikes and coronavirus-related cutbacks. A weakening U.S. dollar, resulting from Friday’s much weaker-than-expected payroll report, pushed base metal prices even higher Friday.

Grain prices were most lower last week in front of this week’s USDA WASDE report. Good weather expectations and better-than-expected harvest completion numbers also weighed on prices. Wheat prices, up strongly over the last few weeks, may have also moved lower because of profit taking. Soybean prices, down less than ½ percent last week, were supported by increased biofuel demand due to rising oil prices.

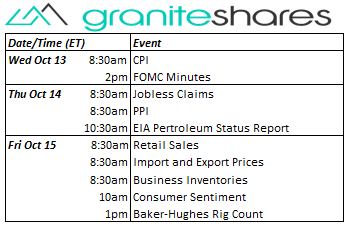

Coming up this week

Another light data-week with inflation numbers, FOMC minutes and retail sales highlighting the week.

Another light data-week with inflation numbers, FOMC minutes and retail sales highlighting the week.- CPI and FOMC minutes on Wednesday.

- Jobless Claims and PPI on Thursday

- Retail Sales, Import and Export Prices, Business Inventories and Consumer Sentiment on Friday.

- EIA Petroleum Status Report on Thursday and Baker-Hughes Rig Count on Friday.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.