Commodities & Precious Metals Weekly Report: Sep 8

Posted:

Key points

Energy prices, except for natural gas prices, were all higher. WTI and Brent Crude oil prices rose 2%, gasoline 3% and gasoil and heating oil prices 6%. Natural gas prices fell 4%.

Energy prices, except for natural gas prices, were all higher. WTI and Brent Crude oil prices rose 2%, gasoline 3% and gasoil and heating oil prices 6%. Natural gas prices fell 4%.- Grain prices were mixed. Wheat and corn prices were up 1%. Soybean prices fell 1%. Soybean oil prices fell 4%.

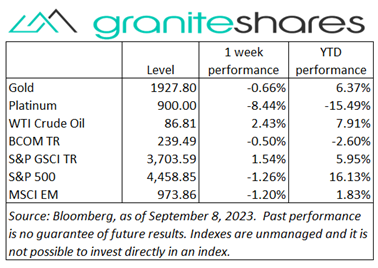

- Spot gold prices fell 1%, spot silver fell 6% and platinum lost 7%.

- Aluminum and zinc prices fell 2%, copper prices fell 4%, nickel prices lost 5% and lead prices dropped 1%.

- The Bloomberg Commodity Index decreased 0.6%, primarily from declining base and precious metal prices. Energy sector gains helped reduce losses for the week.

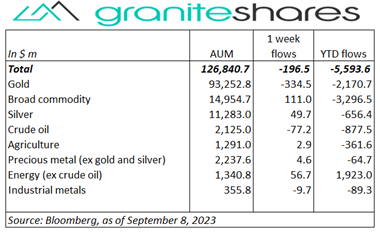

- Net outflows mainly from gold ETPs with smaller amounts from crude oil ETPs. Inflows into broad commodity, silver and energy (ex-crude oil) ETPs.

Commentary

Stock markets moved lower last week with the Nasdaq Composite Index registering the steepest decline versus the S&P 500 Index and the Dow Jones Industrial Average. Concerns of “higher-rates-for-longer” clouded investor outlooks, propelled by lower-than-expected initial jobless claims and a stronger-than-expected ISM Services Index release. Higher oil prices in front of next week’s CPI release added to concerns, increasing expectations of higher-than-desired inflation. Reflecting these concerns, the dollar continued to strengthen and 10-year Treasury rates rose powered by a rise in 10-year inflation expectations. For the week, the S&P 500 Index decreased 1.3% to 4,458.85, the Nasdaq Composite Index dropped 1.9% to 13,761.53, the Dow Jones Industrial Average fell 0.8% to 34,577.28, the 10-year U.S. Treasury rate increased 8bps to 4.26% and the U.S. dollar (as measured by the ICE U.S. Dollar index – DXY) strengthened 0.8%.

Stock markets moved lower last week with the Nasdaq Composite Index registering the steepest decline versus the S&P 500 Index and the Dow Jones Industrial Average. Concerns of “higher-rates-for-longer” clouded investor outlooks, propelled by lower-than-expected initial jobless claims and a stronger-than-expected ISM Services Index release. Higher oil prices in front of next week’s CPI release added to concerns, increasing expectations of higher-than-desired inflation. Reflecting these concerns, the dollar continued to strengthen and 10-year Treasury rates rose powered by a rise in 10-year inflation expectations. For the week, the S&P 500 Index decreased 1.3% to 4,458.85, the Nasdaq Composite Index dropped 1.9% to 13,761.53, the Dow Jones Industrial Average fell 0.8% to 34,577.28, the 10-year U.S. Treasury rate increased 8bps to 4.26% and the U.S. dollar (as measured by the ICE U.S. Dollar index – DXY) strengthened 0.8%.

Oil prices continued their move higher, powered by supply concerns and strong U.S. economic data. Saudi Arabia’s and Russia’s extension of voluntary production cutbacks through the end of the year and sharp, larger-than-expected drawdowns in U.S. inventories significantly contributed to last week’s price rise. Strong U.S. economic data (i.e, lower-than-expected jobless claims and stronger-than-expected ISM Services Index) increased demand expectations, moving prices higher as well. Weak euro zone and Chinese economic data and a strengthening U.S. dollar worked to cap gains.

Spot gold prices ended the week lower with higher rates and a stronger U.S. dollar the primary factor influencing prices. Strong U.S economic data versus weak euro zone and Chinese economic data, set the stage for an appreciating U.S. dollar (particularly versus the Chinese yuan), pressuring prices lower. While expectations of a Fed rate hike this month are near zero, expectations of another hike before year-end remain relatively high, in part driven by climbing oil prices in front of next week’s CPI release. Spot platinum prices fell noticeably more than gold prices, moving lower with base metal prices.

Copper prices also moved lower last week, affected by the same factors influencing gold prices. A strengthening U.S. dollar (especially versus the Chinese yuan), buoyed by contrasting economic data out of the U.S. versus the euro zone and China, provided the major impetus for lower prices.

Grain prices were mostly higher on the week, with soybean prices the exception, falling about ½ percent. Corn prices benefited from continued hot and dry weather forecasts while wheat prices gained on the back of Russian attacks in the Ukraine and no progress on an alternative Black Sea-type agreement. Soybean prices moved lower on declining bean oil prices. Grain prices were somewhat subdued in front of next week’s USDA WASDE report.

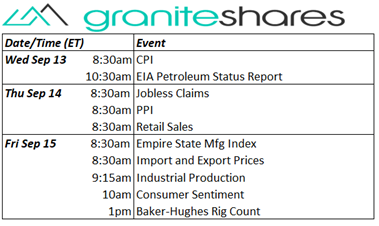

Coming Up This Week

Primary focus is on Wednesday’s CPI release followed by PPI and retail sales on Thursday.

Primary focus is on Wednesday’s CPI release followed by PPI and retail sales on Thursday.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.