Commodities & Precious Metals Weekly Report: Dec 3

Posted:

Key points

Energy prices were predominately lower last week, though gasoil and heating oil prices increased. Natural gas prices were sharply lower, plummeting 24.5%. WTI and Brent crude oil prices fell approximately 2.5% and gasoline prices declined 1.4%. Gasoil prices increased 1.8% and heating oil prices rose 0.4%.

Energy prices were predominately lower last week, though gasoil and heating oil prices increased. Natural gas prices were sharply lower, plummeting 24.5%. WTI and Brent crude oil prices fell approximately 2.5% and gasoline prices declined 1.4%. Gasoil prices increased 1.8% and heating oil prices rose 0.4%.- Grain prices were mainly lower with only soybean prices posting increases. Kansas and Chicago wheat prices fell 5.1% and 4.3%, respectively and corn prices decreased 1.3%. Soybean prices increased 1.2%.

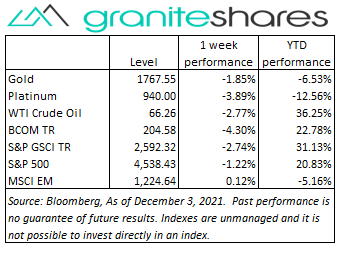

- Precious metal prices were all lower last week. February gold futures prices decreased ¼ percent and February silver futures prices fell 2.8%. Platinum prices fell 3.9%.

- Base metal prices were mixed. Aluminum and nickel prices gained 0.2% and 0.5%, respectively. Copper and zinc prices decreased 0.6% and 1.1%, respectively.

- The Bloomberg Commodity Index fell 4.3% percent predominately due to sharply lower natural gas prices. All sectors of the index posted negative returns.

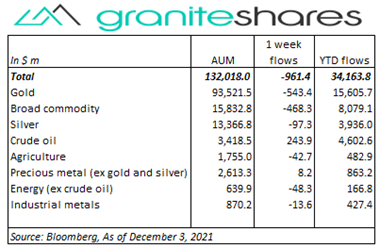

- Almost $1 billion of commodity ETP outflows last week driven primarily by gold and silver ETP outflows. Crude oil ETPs saw inflows of almost $250 million.

Commentary

Another volatile week for U.S. stock markets with uncertainty surrounding the Omicron Covid variant and a potentially more aggressive Fed knee-jerking stock prices lower throughout the week. Monday’s sharp rebound from the previous Friday’s selloff was short-lived with re-emerging Omicron fears compounded by Fed Chairman Powell’s hawkish testimony before Congress on Tuesday. Acknowledging current inflation could no longer be described as “transitory” and positing the pace of tapering could be increased, Chairman Powell’s comments drove stock prices significantly lower Tuesday. Comments from Moderna’s CEO questioning the effectiveness of current vaccines against the Omicron variant added to Covid-related concerns. Wednesday’s report of the U.S’s first Omicron case drove stock markets lower once again though all of Wednesday’s losses were recouped Thursday as investors re-examined Covid-related concerns. Friday’s Non-Farm Payroll report, showing a meager gain of 211,000 jobs but also reporting a lower unemployment rate (combined with an increase in the labor participation rate), seemed to increase investor uncertainty with stock markets again ending sharply lower on the day. The 10-year U.S Treasury rate moved lockstep with stock markets, increasing when stock prices increased and falling when prices fell, reflecting the view a more aggressive Fed would act to slow growth resulting in lower rates and stock prices. Also of note was the Nasdaq Composite Index fared the worst last week, seemingly reflecting greater investor concern of slower growth due to faster Fed tightening than to Omicron. For the week, the S&P 500 Index decreased 1.2% to 4,538.43, the Nasdaq Composite Index fell 2.6% to 15,085.50, the Dow Jones Industrial Average declined 0.9% to 34,579.55, the 10-year U.S. Treasury rate decreased 12bps to 1.36% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) strengthened less than 0.1%.

Another volatile week for U.S. stock markets with uncertainty surrounding the Omicron Covid variant and a potentially more aggressive Fed knee-jerking stock prices lower throughout the week. Monday’s sharp rebound from the previous Friday’s selloff was short-lived with re-emerging Omicron fears compounded by Fed Chairman Powell’s hawkish testimony before Congress on Tuesday. Acknowledging current inflation could no longer be described as “transitory” and positing the pace of tapering could be increased, Chairman Powell’s comments drove stock prices significantly lower Tuesday. Comments from Moderna’s CEO questioning the effectiveness of current vaccines against the Omicron variant added to Covid-related concerns. Wednesday’s report of the U.S’s first Omicron case drove stock markets lower once again though all of Wednesday’s losses were recouped Thursday as investors re-examined Covid-related concerns. Friday’s Non-Farm Payroll report, showing a meager gain of 211,000 jobs but also reporting a lower unemployment rate (combined with an increase in the labor participation rate), seemed to increase investor uncertainty with stock markets again ending sharply lower on the day. The 10-year U.S Treasury rate moved lockstep with stock markets, increasing when stock prices increased and falling when prices fell, reflecting the view a more aggressive Fed would act to slow growth resulting in lower rates and stock prices. Also of note was the Nasdaq Composite Index fared the worst last week, seemingly reflecting greater investor concern of slower growth due to faster Fed tightening than to Omicron. For the week, the S&P 500 Index decreased 1.2% to 4,538.43, the Nasdaq Composite Index fell 2.6% to 15,085.50, the Dow Jones Industrial Average declined 0.9% to 34,579.55, the 10-year U.S. Treasury rate decreased 12bps to 1.36% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) strengthened less than 0.1%.

Oil price movements mirrored U.S. stock market fluctuations, affected similarly to Omicron and Fed tightening concerns. Wednesday’s EIA oil inventory decline was all but ignored due to greater-than-expected increases in gasoline and distillate inventories, helping move oil prices lower. OPEC+, at their meeting Thursday, declined to reduce January’s production increases, initially causing price to fall, but qualified their decision saying they would closely monitor the Omicron situation and meet again if necessary, moving prices higher for the day. Nonetheless, WTI crude oil prices finished the week almost 3% lower. Natural gas prices plunged last week, falling over 24% with almost half that decline occurring Monday. Warmer-than-expected weather in most of the U.S. was the primary reason for the decline in prices.

See-saw week for gold prices, ending the week almost unchanged but fluctuating with on-again/off-again Omicron and Fed tightening concerns. While the 10-year U.S. Treasury rate fell 12bps over the week, influenced by expectations of slowing inflation (as a result of faster Fed tightening), at the same time 10-year U.S. real rates edged lower falling 2bps to -1.11%, indicating expectations for continued, relatively speaking, easy-money Fed monetary policy.

Copper prices moved with oil and stock prices last week, influenced by concerns of weaker demand due to the Omicron Covid variant and and a more aggressive Fed with respect to tightening monetary policy. While copper prices ended the week down about ½ percent, aluminum and nickel prices eked out small gains benefiting from extremely tight supplies.

Grain markets, in general, moved lower with stock and oil prices, hurt by the same macro concerns affecting these other markets. Wheat prices, near a 9-year high last month, also moved lower on profit taking while corn prices, though well of their mid-week lows, suffered from falling oil prices and weakening ethanol demand. Soybean prices ended the week higher, buoyed by hot and dry South America weather concerns.

Coming up this week

Very light data week highlighted by CPI and Consumer Sentiment on Friday.

Very light data week highlighted by CPI and Consumer Sentiment on Friday.- Intl Trade in Goods and Services and Productivity and Costs on Tuesday.

- Jobless Claims on Thursday.

- CPI and Consumer Sentiment on Friday.

- EIA Petroleum Status Report Wednesday and Baker-Hughes Rig Count on Friday.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.