Commoditized Wisdom: Report (Week Ending February 2, 2024)

Posted:

Key points

Energy prices were lower. Oil, heating oil and gasoline prices fell between 5% and 7%. Natural gas prices dropped 4%.

Energy prices were lower. Oil, heating oil and gasoline prices fell between 5% and 7%. Natural gas prices dropped 4%.- Grain prices again were mainly lower. Wheat prices were unchanged, corn prices fell 1% and soybean prices lost 2%.

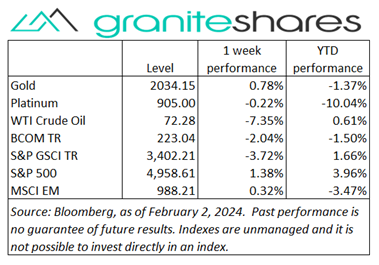

- Spot gold prices rose 1%, spot silver prices fell 1% and spot platinum prices dropped 2%.

- Base metal prices were all lower. Aluminum, copper, nickel and lead prices fell 1% to 3%. Zinc prices fell 5%.

- The Bloomberg Commodity Index fell 2.0% mainly due to losses in the energy and base metals sectors.

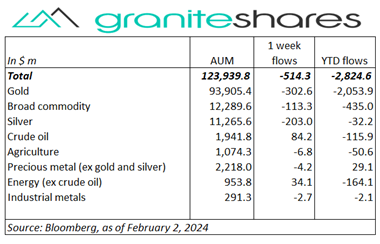

- Outflows from gold, silver and broad commodity ETPs offset slightly by inflows into energy ETPs.

Commentary

A positive but somewhat volatile week with stock markets rising Monday, falling mid-week and then finishing higher. A no-news, momentum rally pushed prices higher Monday in front of a slew of earnings reports, the FOMC announcement and Friday’s payroll report. Markets stalled Tuesday and then dropped markedly Wednesday after Fed Chair Powell all but ruled out a March rate cut and as regional bank concerns re-emerged after New York Community Bank reported a Q4 loss. 10-year Treasury rates, down 10bps through Tuesday, fell another 11bps Wednesday, reacting both to regional bank concerns and to dovish Powell press conference comments supporting expectations of rate cuts this year. Markets rallied strongly Thursday, rising predominantly on the strength of tech stocks and then rallied again Friday on the heels of a surging META stock price and sharply higher AMZN stock price. Friday’s much stronger-than-expected payroll report showing much higher-than-expected jobs creations (as well sharply higher previous-month revisions) seemingly supported stock prices but drove 10-year Treasury yields significantly higher (up 14bps) on increased higher-rates-for-longer expectations. For the week, the S&P 500 Index rose 1.4% to 4,958.61, the Nasdaq Composite Index gained 1.1% to 15,628.95, the Dow Jones Industrial Average increased 1.4% to 38,654.62, the 10-year U.S. Treasury rate fell 12bp to 4.02% and the U.S. dollar (as measured by the ICE U.S. Dollar index – DXY) strengthened 0.5%.

A positive but somewhat volatile week with stock markets rising Monday, falling mid-week and then finishing higher. A no-news, momentum rally pushed prices higher Monday in front of a slew of earnings reports, the FOMC announcement and Friday’s payroll report. Markets stalled Tuesday and then dropped markedly Wednesday after Fed Chair Powell all but ruled out a March rate cut and as regional bank concerns re-emerged after New York Community Bank reported a Q4 loss. 10-year Treasury rates, down 10bps through Tuesday, fell another 11bps Wednesday, reacting both to regional bank concerns and to dovish Powell press conference comments supporting expectations of rate cuts this year. Markets rallied strongly Thursday, rising predominantly on the strength of tech stocks and then rallied again Friday on the heels of a surging META stock price and sharply higher AMZN stock price. Friday’s much stronger-than-expected payroll report showing much higher-than-expected jobs creations (as well sharply higher previous-month revisions) seemingly supported stock prices but drove 10-year Treasury yields significantly higher (up 14bps) on increased higher-rates-for-longer expectations. For the week, the S&P 500 Index rose 1.4% to 4,958.61, the Nasdaq Composite Index gained 1.1% to 15,628.95, the Dow Jones Industrial Average increased 1.4% to 38,654.62, the 10-year U.S. Treasury rate fell 12bp to 4.02% and the U.S. dollar (as measured by the ICE U.S. Dollar index – DXY) strengthened 0.5%.

Oil prices moved lower last week, relinquishing most of the previous week’s gains. Prices moved lower every day but Tuesday last week, weighed down by weak Chinese economic data, strong U.S. economic data and improved production. Contracting Chinese manufacturing activity and the Hong Kong ordered liquidation of Chinese property firm Evergrande lowered demand expectations while a much stronger-than-expected U.S. payroll report added to rate-cut uncertainty, also lowering demand expectations. Increased oil supply due to BP’s Indiana refinery shutdown and to increased U.S. production (resumption of cold-weather related shut downs) added to price weakness. Mideast tensions were responsible for Tuesday’s gains.

Spot gold prices moved higher last week, benefiting primarily from haven buying. Increased Mideast tension in general and the deaths of 3 U.S. soldiers in particular increased gold haven demand, pushing prices higher during the week. Wednesday’s hawkish Powell comments following an as-expected rate decision, acting to pressure prices lower, was offset by renewed regional bank concerns precipitated by New York Community Bank’s unexpected Q4 loss. A larger-than-expected increase in Thursday’s jobless claims bolstered prices while Friday’s much stronger-than-expected payroll report, moving 10-year Treasury rates and the U.S. dollar higher, dragged prices lower. Silver and platinum prices, lower on the week, moved with base metal prices.

Base metal prices fell last week, deflated by weak Chinese economic data and, conversely, strong U.S. economic data. The liquidation of Chinese property firm Evergrande accompanied by the continued contraction of Chinese manufacturing activity contributed to lower prices. Wednesday’s hawkish Powell comments, all but ruling out a March rate cut combined with Friday’s much stronger-than-expected payroll report worked to strengthen the U.S. dollar and increase higher-rates-for-longer expectations, adding to downward price pressure.

Soybean prices finished the week about 2% lower, hurt by good Brazil harvest progress, weaker-than-expected exports and weak Chinese economic data. Wheat prices, basically unchanged on week, benefited from reduced Russian exports in January and concerns India’s wheat production may be hurt by a warmer-than-usual weather this month but hurt by a stronger U.S. dollar. Corn prices, down 1 percent, benefited from short-covering but suffered from a stronger dollar and weak exports.

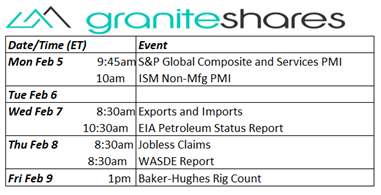

Coming Up This Week

Light week. Composite and services PMIs of note.

Light week. Composite and services PMIs of note.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.