Commodities & Precious Metals Weekly Report: Oct 29

Posted:

Key points

Energy prices were all lower last week. WTI and Brent crude oil prices decreased close to 1% and gasoline and heating oil prices fell about 2.5%. Natural gas prices fell just under ¾ percent.

Energy prices were all lower last week. WTI and Brent crude oil prices decreased close to 1% and gasoline and heating oil prices fell about 2.5%. Natural gas prices fell just under ¾ percent.- Grain prices were all higher again last week. Corn prices jumped 5.6% and soybean prices increased 1.5%. Wheat prices gained between 1.5% and 2.25%.

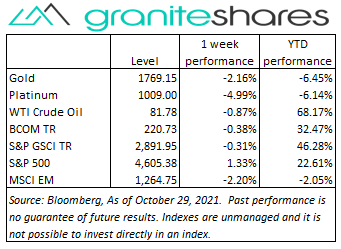

- Precious metal prices ended the week lower. Gold December futures prices fell just under ¾ percent, silver prices dropped 2% and platinum prices lost 5%.

- Base metal prices moved lower as well last week with aluminum prices again falling the most. Aluminum fell 5.3%, copper prices dropped 3% and zinc and nickel prices decreased 1.5% and 1.9%, respectively.

- The Bloomberg Commodity Index moved slightly lower, decreasing 0.4%. Positive performance in the grains and softs sectors was offset by negative performance in the energy and base and precious metals sectors.

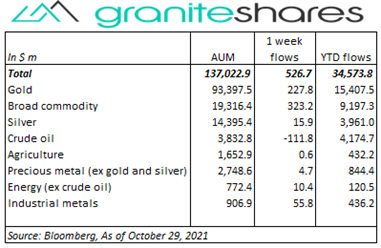

- Decent inflows ($527m) into commodity ETPs last week. Gold ($228m), broad commodity ($323m) and base metal ($56m) ETP inflows were partially offset by crude oil (-$112m) ETP outflows.

Commentary

Another strong week for U.S. stock markets with all three major indexes posting record levels. Strong earnings reports again were the primary factor moving markets higher despite disappointing Apple and Amazon earning releases and a weaker-than-expected increase in GDP. All three major stock indexes moved higher almost every day last week, only pausing Wednesday. Thursday’s weaker-than-expected GDP release (along with Apple’s and Amazon’s disappointing earnings reports) and Friday’s as-expected PCE price index release highlighted concerns surrounding persistently high inflation caused by input/labor shortages and production and shipping bottlenecks and slowing economic activity. 10-year U.S. Treasury rates fell 8bps over the week, perhaps reflecting the growing conviction the Fed will begin moderately tightening monetary policy resulting in slowing economic growth. The U.S dollar, weaker by 0.3% through Thursday, strengthened over 0.8% Friday following the release of the Employment Cost Index and Personal Income and Outlays reports, perhaps reflecting the same conviction. At week’s end, the S&P 500 Index climbed 1.3% to 4,605.38, the Nasdaq Composite Index gained 2.7% to 15,498.40, the Dow Jones Industrial Average increased 0.4% to 35,819.59, the 10-year U.S. Treasury rate fell 8bps to 1.56% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) strengthened 0.5%.

Another strong week for U.S. stock markets with all three major indexes posting record levels. Strong earnings reports again were the primary factor moving markets higher despite disappointing Apple and Amazon earning releases and a weaker-than-expected increase in GDP. All three major stock indexes moved higher almost every day last week, only pausing Wednesday. Thursday’s weaker-than-expected GDP release (along with Apple’s and Amazon’s disappointing earnings reports) and Friday’s as-expected PCE price index release highlighted concerns surrounding persistently high inflation caused by input/labor shortages and production and shipping bottlenecks and slowing economic activity. 10-year U.S. Treasury rates fell 8bps over the week, perhaps reflecting the growing conviction the Fed will begin moderately tightening monetary policy resulting in slowing economic growth. The U.S dollar, weaker by 0.3% through Thursday, strengthened over 0.8% Friday following the release of the Employment Cost Index and Personal Income and Outlays reports, perhaps reflecting the same conviction. At week’s end, the S&P 500 Index climbed 1.3% to 4,605.38, the Nasdaq Composite Index gained 2.7% to 15,498.40, the Dow Jones Industrial Average increased 0.4% to 35,819.59, the 10-year U.S. Treasury rate fell 8bps to 1.56% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) strengthened 0.5%.

Up over 1% through Tuesday on continued strong demand and faltering supply, crude oil prices fell over 2% Wednesday following the EIA reporting a much greater-than-expected increase in U.S. oil inventories. Strong oil demand, exacerbated by skyrocketing natural gas and coal prices, along with restrained production continued to underpin oil prices though an unexpectedly large increase in U.S. oil stocks and renewed concerns of Iranian supply pushed prices lower for the first time in weeks. OPEC+, scheduled to meet Thursday this week, is not expected to increase production.

December gold futures prices moved slightly lower last week, falling over 1% Friday after the release of the Employment Cost Index and PCE Price Index. Concerns of persistent, high inflation and slowing economic growth due to supply chain issues, have pushed 10-year U.S. real rates lower with the Fed cautiously moving toward tightening monetary policy. Friday’s higher-than-expected Employment Cost Index and mostly as-expected PCE Price Index increased expectations of Fed tightening sooner than later, sharply strengthening the U.S. dollar and moving 10-year U.S. Treasury rates slightly lower.

Base metal prices were lower again last week as China continued efforts to move coal prices lower despite historically low copper and aluminum inventory levels. Nickel prices, up almost 3% Monday, ended the week down 1.5% with depressed Chinese steel production reducing Nickel demand in the production stainless steel.

Grain prices were all higher again last week this time with corn prices increasing the most. Strong export and ethanol demand helped move corn prices almost 6% higher last week. Soybean and corn prices also gained on rain-delayed U.S. harvests. Wheat prices moved higher with corn prices but also on tight global supplies and concerns regarding U.S. winter wheat conditions.

Coming up this week

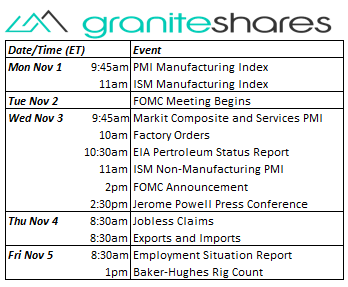

Non-Farm Payroll Report and a2-day FOMC meeting highlight this week’s activity. Manufacturing and services PMI indexes this week as well.

Non-Farm Payroll Report and a2-day FOMC meeting highlight this week’s activity. Manufacturing and services PMI indexes this week as well.- PMI and ISM Manufacturing Indexes on Monday.

- FOMC Meeting begins on Tuesday.

- Markit Composite and Services PMI, Factory Orders, ISM Non-Mfg PMI, FOMC Announcement and Jerome Powell Press Conference on Wednesday.

- Jobless Claims and Exports and Imports on Thursday.

- Employment Situation Report on Friday.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.