Commodities & Precious Metals Weekly Report: Aug 07

Posted:Key points

With the exception of heating oil prices, energy prices were all higher last week. Natural gas surged 24.4%. WTI and Brent crude oil prices increased 2.4% and 2. 1%, respectively. Gasoil and gasoline prices rose 1.1% and 3.1%, respectively. Heating oil prices declined 0.3%.

With the exception of heating oil prices, energy prices were all higher last week. Natural gas surged 24.4%. WTI and Brent crude oil prices increased 2.4% and 2. 1%, respectively. Gasoil and gasoline prices rose 1.1% and 3.1%, respectively. Heating oil prices declined 0.3%.- Grain prices were all lower, led by steep declines in wheat prices. Chicago and Kansas wheat prices dropped 6.7% and 6.1%, respectively. Corn and soybean prices fell 2.6% and 2.8%, respectively.

- Once again, base metal prices, except for copper prices, were all higher. Aluminum, zinc and nickel prices rose 3.3%, 3.6% and 4.3%, respectively. Copper prices fell 2.6%.

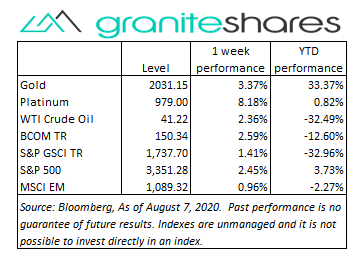

- Precious metal prices were all higher. Gold prices increased 3.4%, silver prices surged 13.3% and platinum prices jumped 8.2%.

- The Bloomberg Commodity Index rose once again last week, increasing 2.59%. The energy and precious metals sectors were primarily responsible for the increase with some contribution provided by the base metal sector as well. The grains sector was the only significant detractor from the index’s performance.

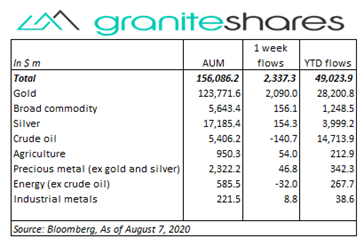

- Commodity ETP total assets continued their climb higher adding $2.3 billion last week. Once again gold ETP inflows were primarily responsible for the increase. Inflows included gold ($2,090.0m), broad commodity ($156.1m) and silver ($154.3m). Crude oil ETPs lost assets again last week, falling $140.7m.

Commentary

Against a backdrop of better-than-expected economic reports and earning results and indications new Covid-19 cases may be falling, U.S. stock markets all moved higher again last week despite concerns over increased U.S.-China frictions and stalled congressional progess on additional coronavirus relief funds. Better-than-expected factory orders and ISM manufacturing and non-manufacturing index numbers combined with lower-than-expected weekly jobless claims and a stronger-than-expected payroll report helped move U.S. equity markets higher. Earning results reported last week were predominantly positive also helping move equity markets higher. Early-in-the-week optimism that congress would reach agreement on additional coronavirus-related relief funds faded as the week ended with no progress, but was slightly ameliorated with the Trump administration announcing the President may take executive action to extend existing programs. Both the U.S. dollar and the 10-year U.S. Treasury rate moved off their lows reached earlier in the week on stronger-than-expected economic reports and signs the number of new Covid-19 cases may be decreasing. At week’s end the S&P 500 Index and Nasdaq Composite index each increased 2.5% to 3,351.28 and 11,010.98, respectively. the 10-year U.S. interest rate increased 4 bps to 57 bps and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) was unchanged.

Against a backdrop of better-than-expected economic reports and earning results and indications new Covid-19 cases may be falling, U.S. stock markets all moved higher again last week despite concerns over increased U.S.-China frictions and stalled congressional progess on additional coronavirus relief funds. Better-than-expected factory orders and ISM manufacturing and non-manufacturing index numbers combined with lower-than-expected weekly jobless claims and a stronger-than-expected payroll report helped move U.S. equity markets higher. Earning results reported last week were predominantly positive also helping move equity markets higher. Early-in-the-week optimism that congress would reach agreement on additional coronavirus-related relief funds faded as the week ended with no progress, but was slightly ameliorated with the Trump administration announcing the President may take executive action to extend existing programs. Both the U.S. dollar and the 10-year U.S. Treasury rate moved off their lows reached earlier in the week on stronger-than-expected economic reports and signs the number of new Covid-19 cases may be decreasing. At week’s end the S&P 500 Index and Nasdaq Composite index each increased 2.5% to 3,351.28 and 11,010.98, respectively. the 10-year U.S. interest rate increased 4 bps to 57 bps and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) was unchanged.

Natural gas prices surged over 24.4% last week, appreciating as a result of hotter-than-expected weather, reduced storage concerns and higher LNG prices. WTI crude oil prices, up nearly 5% through Wednesday on the back of stronger-than-expected economic and earnings reports and lower-than-expected U.S. oil inventories as reported by the EIA, fell over 2% Thursday through Friday amid increased U.S.-China frictions, a congressional impasse on a coronavirus-related relief package and a strengthening U.S. dollar.

Gold prices continued their march higher last week, increasing every day through Thursday, only pausing on Friday after a stronger-than-expected employment report. Supported by a weaker dollar, uncertainty over congressional negotiations on additional coronavirus-related relief funds and increased U.S.-China frictions, gold prices reached another all-time closing high of $2,067.15 per troy ounce on Thursday. Following Friday’s stronger-than-expected employment report and a strengthening U.S. dollar, gold prices moved off their highs, falling 1.7%.

Base metal prices, all higher through Thursday on strong economic reports in the U.S and China and a weakening U.S. dollar, moved lower on Friday after President Trump halted U.S. business dealings with Chinese companies ByteDance and Tencent. Copper prices, for example, up 1.5% through Thursday, fell 4% on Friday following the Trump administration’s announcement.

Oversupply concerns helped move all grain prices lower last week with improved global weather forecasts and higher yield estimates in the U.S. and elsewhere. Grain prices also were affected by uncertainty surrounding next week’s WASDE report, by increased U.S. –China tensions and late-week U.S. dollar strengthening.

Coming up this week

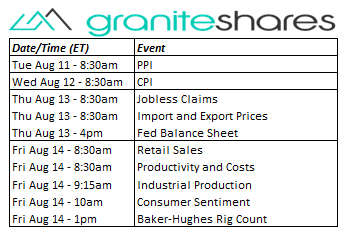

Relatively light week highlighted by inflation reports, retail sales and industrial production.

Relatively light week highlighted by inflation reports, retail sales and industrial production.- PPI on Tuesday.

- CPI on Wednesday.

- Jobless claims, import and export prices and the Fed balance sheet on Thursday.

- Retail sales, productivity and costs, industrial production and consumer sentiment on Friday.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.